A founder I know thought his startup was doing everything right. Revenue was growing. A tax holiday was in place. The cash runway looked safe for the next 12 months. Then a tax computation changed the picture. There was a MAT for startups in India liability he had not planned for.

That is the problem many startups face.

Founders often assume incentives or deductions mean little or no tax, but MAT can still create an unexpected outflow. And when cash leaves early-stage businesses at the wrong time, growth can slow.

The good part? This can be planned for. With the right tax strategy, founders can manage MAT, protect their runway, and avoid surprises. If you’re starting a new venture, choosing the right structure during company registration in Bangalore can play a key role in how your taxes are calculated from day one.

A Quick Look at Startup Tax Benefits

India wants to become a global startup hub. That’s why the government introduced several tax benefits under the tax regime for startups, especially under Section 80-IAC of the Income Tax Act.

Startups recognised by DPIIT (Department for Promotion of Industry and Internal Trade) can claim a 100% tax holiday for three consecutive years, within their first ten years of incorporation. In Budget 2025, this benefit was extended until March 31, 2030, which is a positive move.

But here’s the catch — even if you qualify for a tax holiday, you may still need to pay MAT for startups in India if your firm earns a profit on paper (“book profit”).

What Is MAT for Startups in India and Why Does It Matter?

Minimum Alternate Tax is a way for the government to make sure companies don’t avoid paying taxes entirely by using deductions, exemptions, or incentives. Even if your ordinary tax due is zero, MAT requires you to pay a minimum amount, presently 15% of your book profit.

Here is a simple example.

Assume your startup had a book profit of ₹1 crore in FY 2024-25. Due to tax exemptions under Section 80-IAC, your income tax liability is zero. However, under MAT rules, you’ll still have to pay 15% of ₹1 crore, which is ₹15 lakh as MAT.

Moreover, this generally surprises many founders who assume they won’t owe anything during their exemption period. Understanding MAT for startups in India helps founders plan budgets, manage runway, and negotiate better with investors. You can explore this further in our article on Role of Corporate Advisors in Business Success.

Not sure how MAT impacts your startup finances?

MAT Credit: A Relief for Startups

Here’s where MAT credit comes in. The MAT tax you pay is not gone forever. When your tax holiday expires, you can carry this sum forward and apply it to future tax bills.

Before Budget 2025, startups could carry forward this credit for 10 years. Now, this period has been extended to 15 years, giving more breathing space to early-stage businesses.

So, if you’re paying ₹15 lakh as MAT now, you may get to reduce your tax bill by that amount in any of the next 15 years when you’re paying regular income tax again. This helps to balance things out over time, especially for a growing startup firm that anticipates consistent revenues in the future.

Why Minimum Alternate Tax Still Matters for Startups?

For early-stage startups, cash flow is everything. You may have money on paper, but not in your bank account. If you’re being asked to pay MAT based on book profit, it can affect your runway as well as growth plans.

Moreover, this MAT credit system helps in the long run, but it doesn’t remove the short-term impact. You’re paying real cash today, and that can hurt if you’re not prepared.

Also, the fact that the MAT applies during the Section 80-IAC tax holiday period often leads to confusion. Many startups expect to pay nothing and end up with a sizable tax bill. This is why understanding MAT is crucial if you’re planning your budget, raising funds, or reinvesting profits. Many startups work with experts offering corporate advisory services in India to align tax planning with financial strategy and avoid unexpected liabilities.

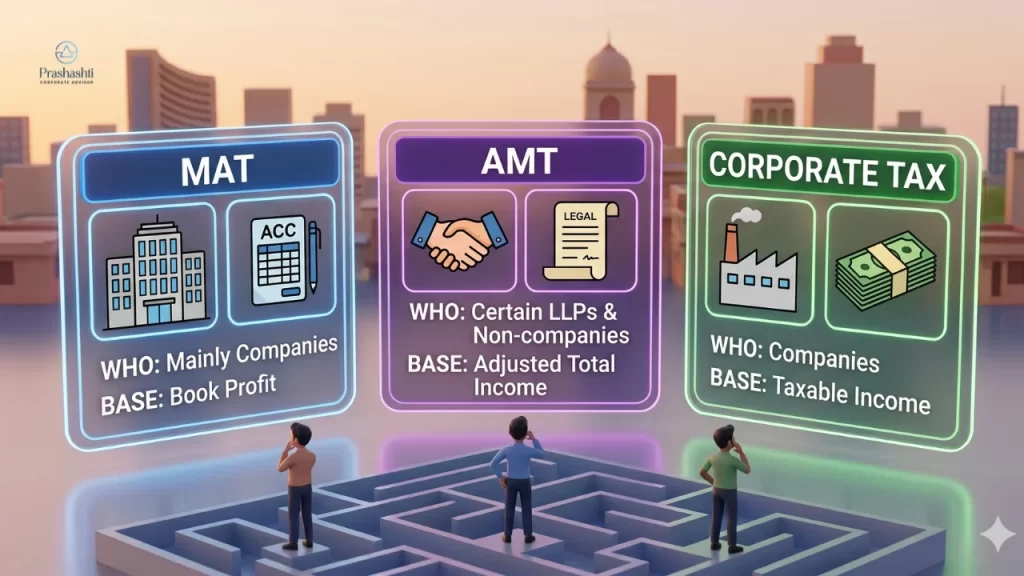

MAT vs AMT vs Corporate Tax

Term | Who it applies to | Base | Rate/idea |

MAT | Mainly companies | Book profit | 15% of the book profit when the normal tax is lower. |

AMT | Some non-company taxpayers, including certain LLPs | Adjusted total income | 18.5% in the tax form rules. |

Corporate tax | Companies under normal rules | Taxable income | Standard tax, compared with MAT to see which is higher. |

Smart Tax Planning Tips to Manage MAT for Startups in India

If your growing startup is heading toward profitability. Making the right structural decisions early, especially during company registration in Bangalore can help optimise your tax position from the beginning. There are a few things you can do to minimise MAT impact:

- Consider alternate tax regimes like Section 115BAA or 115BAB. These provide reduced flat tax rates (22% for domestic enterprises, 15% for manufacturing startups) and can completely free you from MAT. However, you will have to give up other deductions and exemptions, so make your decision carefully.

- Maintain clear accounting records. Keeping your book profits and taxable income cleanly separated helps you track your MAT credit better.

- Include MAT planning in your cash flow projections. If you know you’ll be paying MAT, prepare for it. Include it in your fundraising goals or spending plans.

Stay updated with CBDT notifications and Income Tax rule changes, especially around new clauses like 206, which may redefine what counts as book profit.

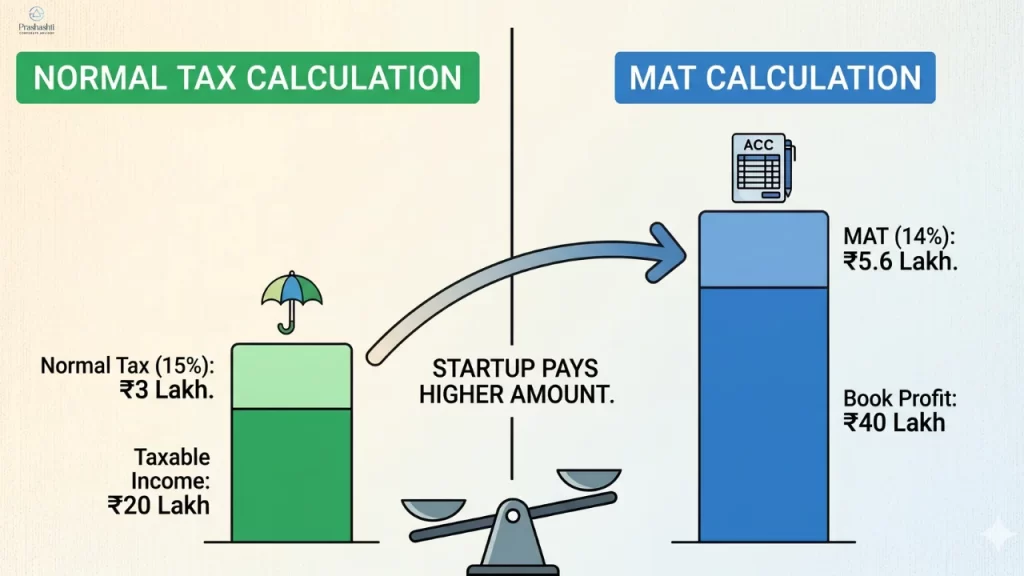

Example: How MAT Is Calculated for a Startup

Let’s make this practical. If you’re still in the early stages, building a strong foundation through a proper startup registration in Karnataka can help you better understand how taxes like MAT will apply as your business grows.

Suppose your startup has:

- Book profit: ₹40 lakh

- Tax under normal provisions: ₹3 lakh

- Applicable MAT rate: 14% (based on 2026 changes)

MAT would be:

0.14×40,00,000=5,60,0000.14 \times 40,00,000 = 5,60,0000.14×40,00,000=5,60,000

So MAT comes to ₹5.6 lakh (before cess and surcharge).

Now compare:

- Normal tax = ₹3 lakh

- MAT = ₹5.6 lakh

Since MAT is higher, the startup may pay MAT.

That means even if deductions reduced your normal tax, you may still have a tax outflow.

That is why founders should never look only at taxable income.

Book profit matters too.

And here is where it gets important.

Under the recent 2026 changes, many businesses are rethinking MAT because fresh MAT credit generation has reportedly changed under the old regime.

Recent Updates & Government Policies on MAT

Any Latest Amendments or Budget Changes

The major development being discussed is the reduction of the MAT rate from 15% to 14% from April 2026. That may reduce some tax burden.

There is also a bigger shift being discussed:

- MAT is increasingly being treated less like a timing tax and more like a final tax under the old regime.

- Fresh MAT credit generation may not work the way it did before.

- Existing credits may face limits in use, depending on regime choices.

Government Stance on Startup Taxation

The government appears focused on:

- Simpler tax structures.

- Moving businesses toward concessional tax regimes.

- Lowering friction in compliance.

- Supporting startups, but with better tax discipline.

The extension of startup-linked tax benefits under Section 80-IAC has also kept the startup tax conversation active. At the same time, MAT rules show that incentives do not always mean zero tax exposure. That balance matters.

Policy Trends Founders Should Watch

Three trends stand out.

1. Shift toward new tax regimes

More companies may be nudged toward Section 115BAA-type structures.

2. Less dependence on MAT credits

This could change long-term tax modelling.

3. Greater focus on cash-flow-based tax planning

Founders may need to treat taxes as part of runway planning, not just year-end compliance.

Common Mistakes Founders Make Regarding MAT for Startups in India

Ignoring MAT in Projections

Many founders forecast revenue, burn, and fundraising, but tax gets missed. That creates blind spots. A runway that looks like 10 months may drop to 9 after MAT. That gap can affect decisions.

Misinterpreting Exemptions

Some assume startup tax benefits mean no tax risk. That can be wrong. Deductions may lower regular tax, but MAT exposure may still remain.

Poor Tax Planning

This often shows up when founders do not compare tax regimes, track book profit adjustments, review MAT credits, or stress-test 115BAA choices.

Expert Tip: “Cash Tax” is not to be confused with “Tax Expense”. If a startup is spending heavily on hardware or merchandise, it can show a profit but have no cash. MAT is based on Book Profit (Accounting Profit), and you could have to pay ₹7 lakh tax to the department, although you have just a bank balance of ₹2 lakh. “Always align your fundraising milestones with your tax calendar.

Why Founders Should Plan for MAT Early?

For many growing startups, the real challenge isn’t just launching a business, it’s navigating what comes after. One such roadblock is the MAT. Even during tax holiday periods, MAT can cut into cash reserves and catch founders off guard.

But this isn’t a dead end. With recent policy changes like the extended credit period and flexible tax regimes for early-stage companies, they now have better ways to manage their tax exposure, if they know where to look.

Prashasthi Corporate collaborates closely with startups to help them understand these issues early on. Whether it’s selecting the right structure, planning for MAT, or staying compliant as you grow, our goal is simple: assist you in making informed decisions from the start, so taxes never slow you down.

Pingback: Government Schemes Startups in India 2026: Funding & Seed Grants

Pingback: Tax Audit Requirements in India: Limits, 5% Rule & Key Mistakes