How Recent Amendments to Corporate Tax is Impacting Compliances in 2026

India’s corporate tax situation took a sharp turn in 2025. Those shifts are not coming, but they are the operating reality for every company that files in FY 2026-27, a year later.

Corporate tax rules have changed as a result of the most recent Union Budget and Finance Act. Startups have more breathing room. Big firms face tighter rules on interest and cross-border deals. Filing deadlines, penalties, and global standards? They’re all part of the mix now.

In this blog, we break down what’s changed, why it matters for your business, and how to stay ahead without losing your mind or money.

Major Corporate Tax Changes Still Impacting Businesses in 2026

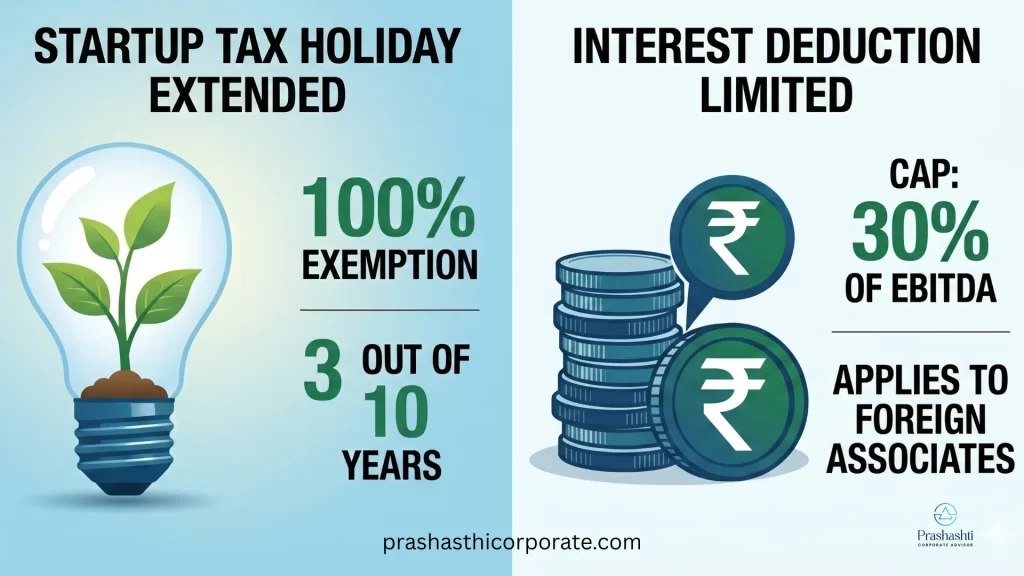

1. Startup Tax Holiday Extended Until 2030

Startups registered up to April 1, 2030, can now claim a 100% tax exemption for 3 out of their first 10 years. Earlier, this benefit was only for startups set up before March 31, 2024.

This change helps new businesses save money during their early growth years. To claim this benefit, startups must meet eligibility criteria, including certification from the government and a turnover limit.

2. Interest Deduction is Limited

Companies that spend more over ₹1 crore in interest to associated foreign parties can now deduct just 30% of their EBITDA as interest expenditure.

This prevents tax avoidance by over-reporting of interest payments. If a company crosses the cap, the extra interest can’t be deducted, though it can be carried forward for eight years.

This law mostly impacts enterprises that borrow substantially from overseas group companies.

3. Global Minimum Tax in Sight

India is preparing to adopt the OECD’s global minimum tax rules. Under this framework, large multinationals must pay at least 15% tax, no matter where they are based.

If a company’s Indian unit pays less than this, the parent country can charge extra tax to fill the gap.

While it has not yet been enforced in India, businesses having international ties should be aware of it.

4. A Simpler Tax Law

The government has tabled a new income tax bill. It intends to replace the outdated Income Tax Act of 1961 with something simpler and shorter.

The new law uses easy language, reduces the number of sections, and removes outdated terms. The goal is to make tax filing clearer and reduce legal confusion, especially for small and medium businesses.

Corporate Tax Filing & Compliance Updates for 2026

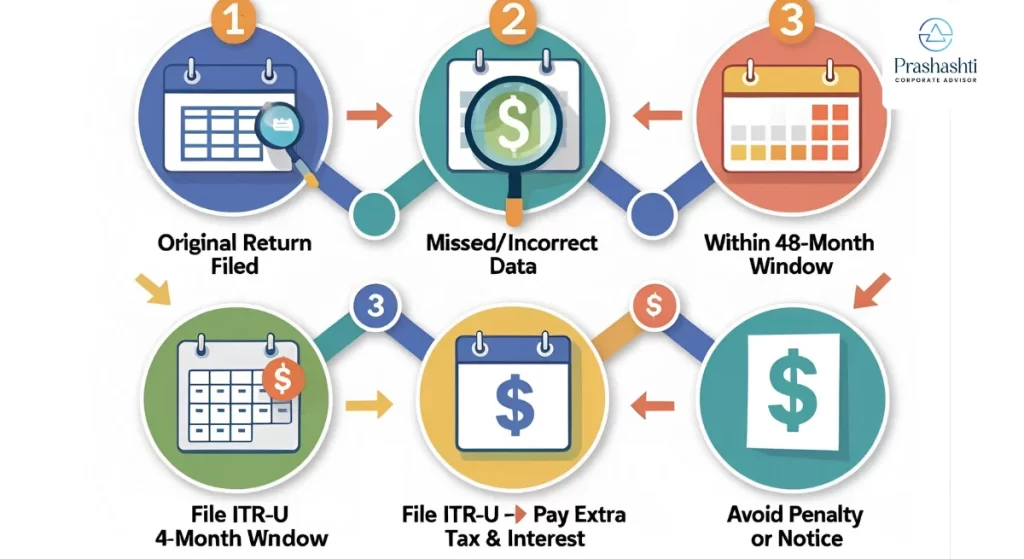

1. ITR-U Window Doubled

Companies now have 48 months (instead of 24) to file an updated return (called ITR-U). If a company overlooks anything or makes an error on its first return, it can correct it willingly and avoid penalties by paying the additional tax and interest.

This extension is part of a broader shift toward improving Corporate Tax compliance by encouraging self-correction and reducing disputes with tax authorities. Under Budget 2026 proposals, ITR-U can now be filed even after reassessment proceedings have begun, with a 10% additional tax, to reduce litigation

2. ITR Due Date Extended

For FY 2025-26 — ITR-1 and ITR-2 taxpayers should file their returns by July 31, 2026, and cases of non-audit business should be filed by August 31, 2026. Revised returns are also now due by March 31 of the following tax year, instead of December 31.

3. Faster Filings and Tiered Penalties

Changes to the Companies Act require firms to file key documents, such as resolutions or financial updates, within 7 days. Previously, the maximum was thirty days.

Penalties are now tier-based. Smaller companies may pay less, but repeat or large violations attract higher fines.

Transfer Pricing and TDS/TCS Compliance Changes in 2026

3-Year Block for Pricing Tests

Businesses engaged in cross-border transactions can now test their transfer pricing over a 3-year block instead of every year. This option is live, effective April 1, 2026, but it requires a conscious opt-in. Companies are required to file Form 46 with an accountant’s certificate in Form 47 certifying that the nature of the transaction and circumstances of the business have not substantially changed, before 30 June of the third tax year.

However, if there are big changes in business structure or profit levels, locking in a method for three years may not be suitable. As corporate tax rules evolve, this approach provides some flexibility for businesses, but it also necessitates careful preparation.

TDS/TCS Thresholds Raised

Thresholds for deducting and collecting tax at source have been increased for payments like rent and professional fees. This gives relief to smaller payments and helps reduce unnecessary deductions. But the more significant 2026 change is structural – the entire 194-series is retired. From 1st April 2026, the TDS and TCS liabilities will be covered by three new consolidated sections i.e. 392 for salary, 393 for all other payments and 394 for TCS.

Companies also need to update their systems to ensure the correct rates are applied.

Equalisation Levy Removed

From April 1, 2025, the 6% tax on foreign digital ads is eliminated. There will be no additional expenses when advertising on platforms such as Google or Meta.

It also means fewer tax issues and improved compliance with worldwide regulations.

Need help understanding the latest corporate tax changes?

Why Corporate Tax Compliance Matters More in 2026?

Back in 2025, these corporate tax changes felt like another round of government updates. In 2026, they’re no longer “new changes”; they’re the system businesses are already working under.

The old Income Tax Act of 1961 is gone. From April 1, 2026, companies are dealing with the new Income Tax Act 2025, which has a simpler structure and cleaner language. But the transition has not been as easy as many had hoped. Finance teams continue to update references to old sections, forms, and payment codes that no longer exist.

And the effects aren’t the same for everyone. Startups formed till March 31, 2030, can still receive a 3-year tax holiday under section 80-IAC, if documents and approvals are in order. We are seeing actual EBITDA interest cap submissions from mid-size firms already. Multinationals are investing more time on tax structure, disclosures and cross-border compliance as India draws closer to the OECD Pillar Two framework.

The good news was that the Finance Act 2026 reduced penalties for less serious defaults. Today, tax compliance has become a chain reaction. Miss one deadline and many filings could be at risk.

Staying Ahead of Corporate Tax Compliance in India

The 2026 amendments to Corporate Tax laws include more than just new rates; they also introduce a paradigm shift. The government is rewarding honest, early compliance while striving for simpler, more predictable rules.

These improvements can make your tax journey go more smoothly if you plan ahead of time, stay aware, and keep correct documents. It’s not just about avoiding penalties, it’s about building a business that’s ready for both local and global expectations.

Teams like Prashasthi Corporate assist businesses in navigating change with clarity and confidence.