You get a pay raise and feel happy about it. Then, you decide to check your EPFO passbook. Your EPF balance has increased as you predicted. But then you look at the pension part, and it barely seems to have changed. That’s when the doubt kicks in. Shouldn’t your pension contribution increase too? Did something go wrong, or is this just how it works?

A lot of people run into this confusion. The thing is, EPS pension calculation doesn’t work the same way as EPF, even though both come from the same PF deduction. There are a few rules in the background, like how the employer’s share is split and the ₹15,000 salary limit, that quietly affect how much actually goes into your pension.

In this blog, we’ll walk through how your PF contribution is divided, how the EPS part is calculated, and what all of this means for the pension you’ll eventually receive.

“On 29 June 2026, the Ministry of Labour and Employment formally superseded the Employees’ Pension Scheme, 1995 and the Employees’ Family Pension Scheme, 1971 with the Employees’ Pension Scheme, 2026 (Notification G.S.R. 527(E)), issued under Section 15(1)(b) of the Code on Social Security, 2020. The new scheme took effect the same day it was published in the Official Gazette.”

What Is the Employee Pension Scheme (EPS)?

The Employee Pension Program (EPS), also referred to as the EPS 95 scheme, is a government-sponsored retirement program that was established in 1995. This is taken care of by the Employees’ Provident Fund Organisation (EPFO), and it aims at delivering you a regular monthly income after retirement.

Most salaried people are familiar with EPF because they see that deduction on their payslip every month. But what many don’t realise is that a part of the employer’s contribution actually goes into EPS. This is where a lot of confusion begins, especially when people try to match their salary slip with their EPFO passbook.

Here’s the simple way to think about it:

- EPF helps you build a lump sum over time.

- EPS provides a fixed monthly pension after retirement.

You don’t get a big return from EPS, but a fixed monthly sum after retirement, depending on a formula. That’s why EPS pension calculation is important to know if you want to have a fair estimate of your future income.

EPS is meant to offer financial help after retirement. It also includes events like disability or death, with benefits such:

- Family pension

- Widow pension

- Orphan pension

These pension benefits are supposed to give financial stability in case things don’t go as planned. You can verify eligibility rules and use the official pension estimator directly on the EPFO Member Portal.

EPF vs EPS: What's the Difference?

Here’s a quick comparison:

Feature | EPF | EPS |

Objective | Retirement savings | Monthly pension after retirement |

Contribution | Employee and employer | Employer only |

Interest | Earns annual EPF interest | No interest is credited |

Withdrawal | Lump-sum withdrawal allowed as per rules | Monthly pension after eligibility |

Retirement Benefit | Corpus accumulated over the years | Lifetime monthly pension |

How the 12% EPF Contribution Actually Works?

One of the most common misunderstandings is that both your contribution and your employer’s contribution go entirely into EPF. That’s not true.

Every month:

- You contribute 12% of Basic Salary + DA

- Your employer also contributes 12% of Basic Salary + DA. Learn more about how the PF contribution of employer is calculated.

But the allocation is different.

Employee Contribution

- You contribute 12% of Basic Salary + DA. Employees who wish to build a larger retirement corpus can also opt for VPF contribution.

- 100% of this goes into EPF

- 0% goes into EPS

Employer Contribution

Your employer’s 12% contribution is split as follows:

- 8.33% EPS contribution → goes into EPS

- 3.67% EPF employer contribution → goes into EPF

Additionally:

- Employers pay administrative charges separately.

- These charges are not deducted from your salary.

Here’s a summary:

Contribution | EPF | EPS |

Employee 12% | 12% | 0% |

Employer 12% | 3.67% EPF employer contribution | 8.33% EPS contribution |

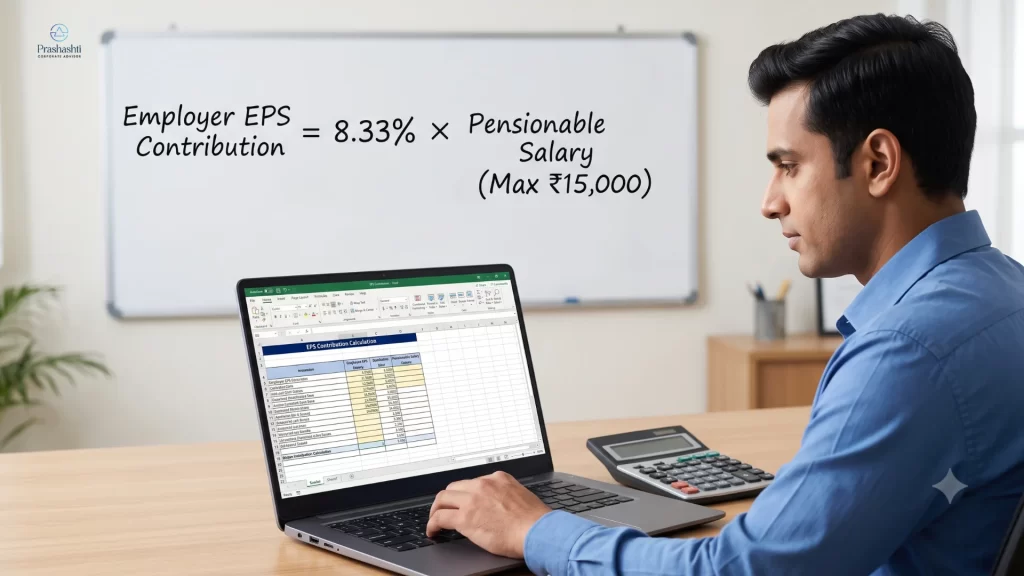

How the EPS Pension Calculation Formula Works?

Now that you know how the employer’s contribution is split, let’s look at how the EPS portion is calculated.

The formula is: Employer EPS Contribution = 8.33% × Pensionable Salary.

However, there’s an important detail to understand.

Understanding the EPS Wage Ceiling Nuance

Under standard rules:

- EPS contributions are calculated only up to ₹15,000 per month.

- Even if your salary is higher, the contribution is capped.

Let’s look at examples:

Monthly Salary | EPS Calculated On | Monthly EPS Contribution |

₹12,000 | ₹12,000 | ₹999.60 |

₹15,000 | ₹15,000 | ₹1,249.50 |

₹30,000 | ₹15,000* | ₹1,249.50 |

This explains why:

- Many employees see EPS contributions around ₹1,250.

- Contributions don’t increase even when salary increases.

Key points to remember:

- The ₹15,000 limit is the existing standard ceiling.

- It has been updated from time to time.

- Higher Pension situations may be treated differently.

Besides, EPS is not same as EPF:

- It is not an investment

- It does not earn interest

- It does not grow like EPF balance

Instead, your pension depends on:

- Your salary (within limits)

- Your years of service

Expert Insight: In our payroll compliance work, alongside payment of ESIC, the EPS miscalculations we catch most often aren’t dramatic.; they’re small, repeated errors that compound over years of service. The two we flag most: employers applying the 8.33%/3.67% split to gross salary instead of Basic + DA, and EPS being calculated on full salary for employees who joined after the ₹15,000 ceiling rules applied to them. Neither shows up on a payslip as an obvious error; it only surfaces years later when someone compares their EPFO passbook to what they expected. If you’ve changed employers more than twice, it’s worth having your service record and contribution history reviewed rather than assuming payroll got it right every time.

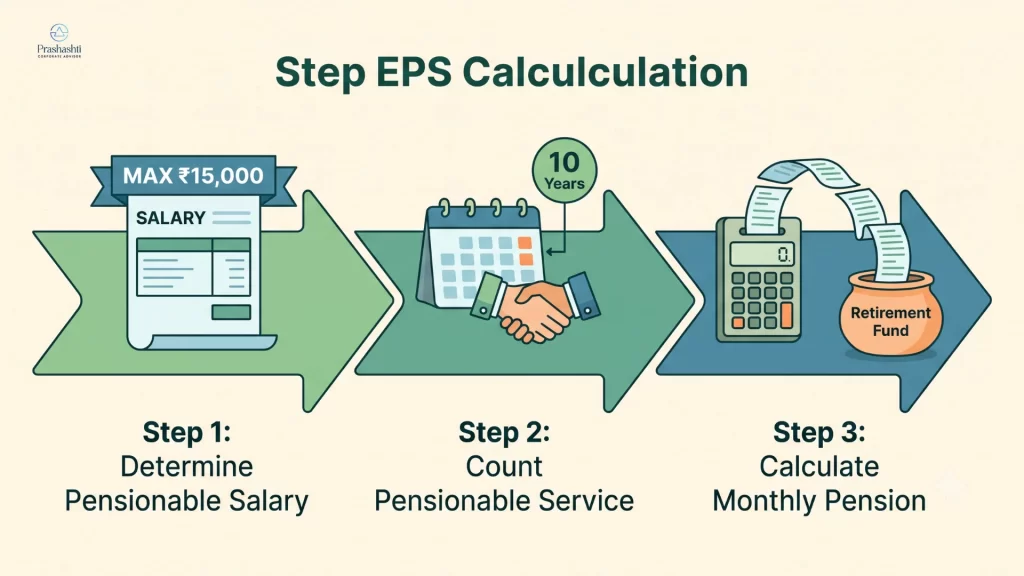

EPS Pension Calculation Formula (Step-by-Step Walkthrough)

Alright, now that we’ve covered how contributions work, let’s get to the part most people actually care about: how your pension is calculated.

The formula EPFO uses is pretty simple on paper:

Monthly Pension = Pensionable Salary × Pensionable Service ÷ 70

Step 1: Understand Your Pensionable Salary

Your pensionable wage is the salary used by EPFO in calculating your pension.

The thing is, it’s ₹15,000 at most for most people.

So even whether your actual basic pay is ₹25,000 or ₹40,000, for the pension calculation, ₹15,000 is usually still used (unless you’re under the Higher Pension option).

Step 2: Count Your Pensionable Service

This just means the number of years you have contributed to EPS.

You must have served for at least 10 years to qualify for a monthly pension. If you quit before then you won’t earn a conventional pension (but there are alternative choices depending on your circumstance).

Step 3: Plug the Numbers into the Formula

Once you know your salary (₹15,000 in most cases) and your years of service, just apply the formula:

Monthly Pension = Pensionable Salary × Pensionable Service ÷ 70

That gives you a rough idea of what you’ll receive every month under the EPS 95 scheme. For a member-specific estimate based on your actual EPFO records, use the official EPFO Pension Calculator; note that EPFO itself states these calculations are illustrative only, and the amount actually processed by your regional EPFO office is final.

EPS Pension Calculation Examples

Let’s make this more real with a few simple examples.

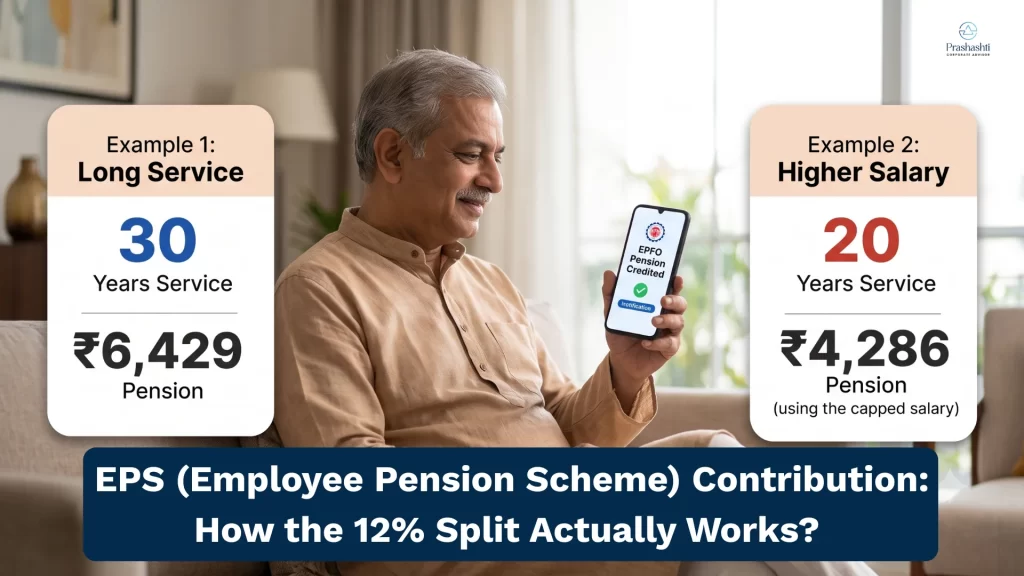

Example 1: Salary Rs.15,000 and 30 years of service

Now consider someone who worked longer, say 30 years:

Monthly Pension = ₹15,000 × 30/70 = ₹6,429 (approximate)

Same pay, but longer years = bigger pension.

Example 3: Salary ₹30,000 Per Month

Say a person makes 30,000 per month. You might think their pension will be calculated on ₹30,000, but that’s not how it works.

Unless they’ve opted for the Higher Pension scheme, EPFO still considers only ₹15,000.

12% EPF Contribution with Salary Examples

Here’s how contributions look at different salary levels:

Monthly Salary | Employee EPF | Employer EPF | Employer EPS |

₹12,000 | ₹1,440 | ₹440.40 | ₹999.60 |

₹15,000 | ₹1,800 | ₹550.50 | ₹1,249.50 |

₹20,000 | ₹2,400 | ₹1,150 | ₹1,249.50* |

₹30,000 | ₹3,600 | ₹2,350 | ₹1,249.50* |

EPFO Mythbusting: Is the Minimum Pension Really ₹7,500 Now?

In May 2026, a letter claiming the minimum EPS pension had been officially hiked from ₹1,000 to ₹7,500, effective 1 May 2026, went viral across WhatsApp and social media. EPFO publicly confirmed via its official handle that the letter was fake.

Here’s the actual, verified status as of mid-2026:

- The minimum monthly pension under EPS remains ₹1,000, unchanged since September 2014.

- The government has acknowledged, in a formal reply to Parliament, that the Employees’ Pension Fund carries an actuarial deficit (as valued on 31 March 2019), and that the ₹1,000 floor is maintained through budgetary support rather than being a naturally earned benefit.

- Proposals to raise it, figures ranging from ₹1,500 to ₹7,500 have circulated, remain under discussion, with no notification issued.

The practical takeaway for readers: don’t trust forwarded pension “notifications.” Check EPFO’s verified handle or epfindia.gov.in directly before acting on any viral claim about pension hikes.

Common Payroll Errors That Affect EPS Contributions

Even though payroll is mostly automated these days, mistakes still happen, and they can affect your pension later.

- One common misunderstanding is thinking that your 12% contribution also goes into EPS. It doesn’t. Your entire share goes only to EPF.

- Another issue is ignoring the ₹15,000 limit. Some employers mistakenly calculate EPS on full salary, which can create problems later.

- Sometimes contributions are based on gross salary instead of basic + DA which is not accurate.

- It’s also possible to have faults in software where the employer’s contribution isn’t split correctly between EPF and EPS. If that happens, you can see unusual entries in your EPFO passbook.

- Errors in higher pension processing, missing service records after changing jobs or inaccurate UAN details might also influence your future pension.

Who Is Eligible for EPS?

If you’re part of EPF, you’re usually automatically part of EPS too. This generally begins once your employer completes your PF registration online.

But to actually receive a monthly pension, you need to complete at least 10 years of service and reach the retirement age defined under the scheme.

If you leave before 10 years, you won’t get a regular pension, though there may be other benefits depending on your situation.

EPS also supports your family. If something happens to the member, benefits like widow pension or children’s pension may be offered.

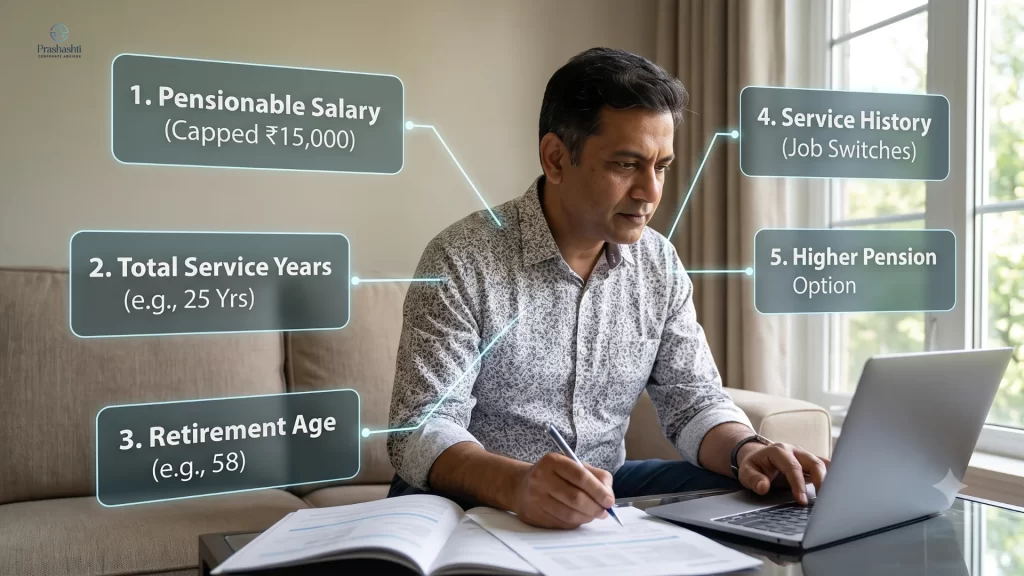

Factors That Affect Your Pension Benefits

Your pension amount mainly depends on a few key things:

- Your pensionable salary (usually capped at ₹15,000).

- Your total years of service.

- Your retirement age (early retirement can reduce pension).

- Whether you’re under the Higher Pension option.

- Accuracy of your service records.

If you have switched jobs many times, ensure your UAN is linked properly and your service history is updated.

How to Check Your EPS Contribution in the EPFO Passbook?

You can check it yourself to see if everything is being calculated correctly or not.

- Log in to the EPFO Member e-Sewa Portal using your UAN.

- Open your EPFO e-passbook and select your member ID to see monthly contributions.

- Cross-check your service history, especially if you’ve switched jobs, total service years directly affect your EPS pension calculation.

EPS Pension Calculation: A Final Word from Prashasthi Corporate

EPS pension calculation could seem confusing at first, especially when trying to understand your income slip or EPFO passbook. But once you understand how the employer’s contribution is divided, what the wage ceiling means, and how your pension is actually worked out, things start to become clearer. It also helps you set more realistic expectations for your retirement.

If you ever feel trapped or unsure regarding EPF, EPS, ESIC benefits, or payroll guidelines it’s fine to ask for advice. Companies like Prashasthi Corporate take care of these things on a regular basis and can help you through the process in a simple and practical manner without making it sound complicated.

Disclaimer: This article is for general informational purposes only and does not constitute financial, tax, or legal advice. EPS/EPF rules, wage ceilings, and pension formulas are subject to periodic government notification. Please verify your specific entitlements on the official EPFO portal or consult a qualified advisor before making financial decisions.