You know that feeling when your income is credited and you feel wonderful for a second… and then you start thinking about the future? Rent, bills, daily expenses, everything keeps going up. And somewhere in the back of your mind, there’s this quiet worry: “Is my EPF really enough for retirement?” That’s where a VPF contribution comes in. It’s not something most people talk about, but it’s actually one of the simplest ways to save more without changing much in your routine.

The thing is, a lot of people have heard the term but don’t truly know what it means. Some think it’s complicated, some say it’s just like EPF, and many just disregard it altogether.

So in this blog, we will decode in simple language what a VPF contribution truly is, how it works, who should consider it, and if it makes sense for you compared to other options like PPF or NPS. We have also added a few items that most VPF guides will not tell you, like a simple way to determine if your contribution will attract tax, what truly happens if you withdraw early, and what is changing at EPFO in 2026.

What is a Voluntary Provident Fund (VPF)?

If you’re already contributing to EPF and feel like you could save a bit more for the future, that’s where the Voluntary Provident Fund (VPF) comes in. It’s basically an extension of your Employee Provident Fund (EPF).

It is a government-backed investment because it is all administered under the EPF system by the Employees’ Provident Fund Organisation (EPFO), a statutory agency under the Ministry of Labour and Employment. So a lot of people like it when they need something safe and reliable for their retirement savings.

What is a VPF Contribution?

A VPF contribution is simply the extra amount you decide to put into your EPF account over and above the employer PF contribution.

Let’s say your basic salary plus DA is ₹50,000. You’re already contributing 12% to EPF. Now, if you feel like saving more, you can choose to add another percentage as a voluntary provident fund contribution. This is withdrawn from your salary every month automatically.

Expert Insight: We increasingly see young professionals in their first 2-3 years of employment treat EPF as a payroll deduction they don’t think about, rather than as the base layer of their retirement plan. Given that nearly 6 in 10 new EPFO subscribers are under 25, this is precisely the stage where even a modest VPF top-up, say 5-10% of basic pay, has the longest possible runway to compound at a stable, government-backed rate. The earlier this conversation happens, the less it costs to build a meaningful corpus later.

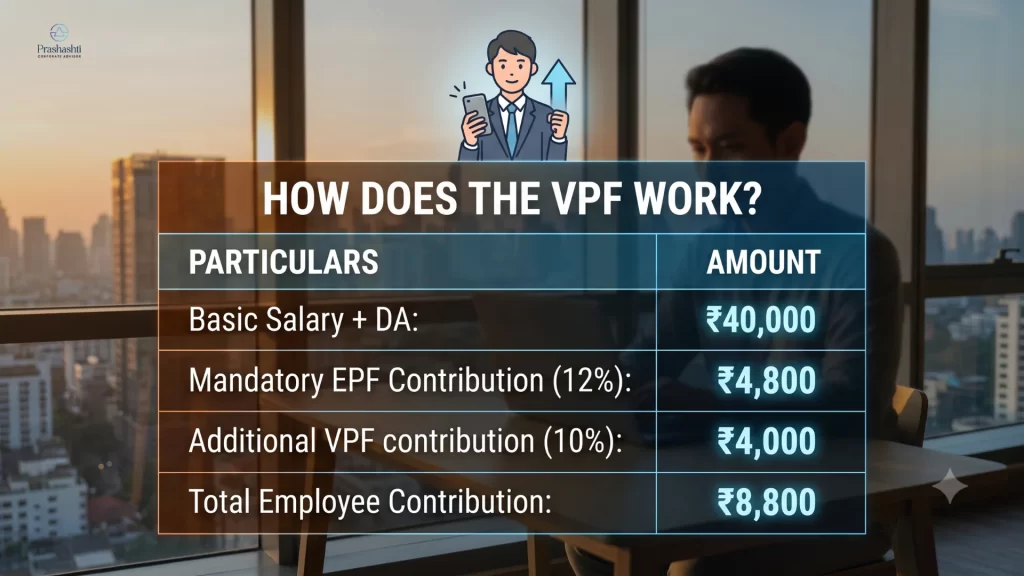

How Does The VPF Work?

Let’s see this with a simple example.

Particulars | Amount |

Basic Salary + DA. | ₹40,000 |

Mandatory EPF Contribution (12%). | ₹4,800 |

Additional VPF contribution (10%). | ₹4,000 |

Total Employee Contribution. | ₹8,800 |

Who Can Make a VPF Contribution?

VPF isn’t open to everyone. Since it’s tied to EPF account, only people who already have an EPF account can opt for it.

- Government employees who are part of EPF can also use this option.

- But if you’re self-employed, freelancing or running your own business, VPF isn’t available as there’s no EPF account to link it to.

- It’s also worth noting that you do have some freedom in how much you put in. There are circumstances where you can even contribute up to 100% of your basic pay and DA, but that depends upon the payroll laws of your organization.

The Prashasthi VPF Allocation Matrix: How Much Should You Actually Contribute?

Your Situation | Tax Regime | Liquidity Need (next 3-5 yrs) | Suggested VPF Range |

Early-career (22-30), few dependents | Old regime | Low | 15-25% of Basic+DA. |

Early-career (22-30), few dependents | New regime | Low-Medium | 5-10% (tax benefit doesn’t apply, treat as pure savings discipline). |

Mid-career (30-45), home loan/children’s education ahead. | Old regime | Medium-High | 8-15%, supplemented by more liquid instruments. |

Mid-career (30-45) | New regime | Medium-High | 5-8%, prioritise liquid/market instruments for near-term goals. |

Pre-retirement (45+), 80C limit unused elsewhere. | Old regime | Low | 20-30%+ (maximise stable, tax-free compounding in the final stretch). |

Please note: Indicative ranges based on typical client profiles we advise on; not a substitute for a personalised assessment of your income, dependents, and existing 80C/123 utilisation.

Key Features and VPF Benefits

A lot of people prefer VPF because it’s simple, safe, and doesn’t require constant monitoring. Once you set it up, it runs on autopilot.

Build a Larger Retirement Savings Corpus

Even small increases in your monthly VPF contribution can add up over time. Because of compounding, the longer you stay invested, the more your savings grow.

If you’re someone who prefers steady, predictable growth instead of market ups and downs, VPF can be a solid provident fund investment.

Secure Government-Backed Investment

Market movements aren’t something you have to worry about every day, way stocks or mutual funds are.

Attractive Interest Rate

One of the biggest VPF benefits is the interest rate. It’s the same as EPF, which is usually higher than many traditional fixed-income options.

For FY 2025-26, EPFO’s Central Board of Trustees retained the rate at 8.25%, the third consecutive year at this level, and it has since been ratified by the government. Notably, EPFO has also sped up disbursal this year: interest for FY 2025-26 is being auto-processed and credited to nearly 34 crore member accounts by 15 July 2026 through its new Centralised IT Enabled Services (CITES) platform, well ahead of the October-November timelines subscribers were used to in previous years. You can verify your own credit status directly on the EPFO Member Portal or the UMANG app.

Tax-Saving Investment Under Section 80C

If you’re following the old tax regime, your VPF contribution can help you save tax.

It qualifies for a Section 80C deduction, which means you can reduce your taxable income while also building your savings. It’s a win-win, especially if you haven’t fully used your 80C limit yet.

Automatic Salary Deductions

One underestimated benefit is how easy it is. The payment is taken straight from your salary so you don’t have to remember to contribute each month.

Low-Risk Provident Fund Investment

If your goal is long-term retirement savings without too much uncertainty, VPF offers a good balance of safety and steady returns.

VPF Interest Rate and Tax Benefits

The interest you earn on your VPF contribution is exactly the same as EPF since both sit in the same account. The EPFO announces this rate every year, and for FY 2025-26, it stands at 8.25%.

Even though the interest is credited once a year, it’s calculated on your monthly balance. So your money keeps growing throughout the year.

From a tax point of view, VPF is quite beneficial, especially under the old tax regime. You can get a Section 80C deduction for your payments, which lowers your taxable income.

That said, there’s one thing to watch out for. If your total contribution (including EPF and VPF) goes beyond ₹2.5 lakh in a year, the interest earned on the excess amount may be taxable. This rule was introduced to limit tax-free accumulation on very large balances.

Also, if you’ve opted for the new tax regime, you won’t be able to claim the Section 80C deduction, which is why many employees seek corporate advisory services to evaluate which tax regime and retirement strategy best suit their financial goals.

Expert Insight: The regime question comes up in almost every advisory conversation we have with salaried clients. VPF’s tax deduction only has value if you’re actually on the old regime, so before increasing your VPF contribution purely for tax-saving purposes, run the numbers on both regimes for your specific salary structure first. We’ve seen employees over-contribute to VPF under the old regime out of habit, when the new regime’s lower slab rates would have left them better off overall, even without the 80C benefit. It’s a five-minute calculation that’s worth doing every year, not just once.

Section 80C is being renumbered: “The Income Tax Act, 2025, which has come into force from 1 April 2026, replaces the six-decade-old Income Tax Act, 1961, and applies from Tax Year 2026-27 onwards. Section 80C, which is quite well known, has been re-numbered as Section 123 and the additional deduction for NPS which was formerly under Section 80CCD(1B) is now under Section 124 under the new Act. The limit of ₹1.5 lakh deduction remains the same. Just the section number and legal terminology has changed (Tax Year instead of Previous Year/Assessment Year). If you are filing returns or revising salary declarations for FY 2026-27 onwards, your Form 16 and ITR utility may refer to Section 123 instead of 80C, do not panic, it is the same benefit in a different name.”

How to Verify Your VPF Contribution Is Reflecting Correctly?

VPF deduction errors are more common than you think, and with EPFO’s account transfer happening until 2025-26, it’s worth carefully checking.

- To see the EPFO passbook in a mobile-friendly manner, log in to the EPFO Member Portal with your UAN and password or the UMANG app.

- Check the e-passbook under the “View” option. Your VPF contribution will be shown as part of the employee share, so check the amount deducted every month with your payslip.

- Update your KYC as “Verified” (not “Pending”) for Aadhaar, PAN and bank account. EPFO’s new Centralised IT Enabled Services (CITES) system has indicated that unverified KYC can cause delay in visibility of interest credit and any future withdrawal claim.

- If contributions look off, raise it with payroll first (VPF is employer-processed), and escalate to EPFO’s grievance portal only if the employer doesn’t resolve it.

How Employees Opt In Via Employer ?

Getting started with a VPF contribution is actually pretty easy. The good part is that your employer takes care of most of the process, so you don’t have to deal with anything complicated.

- The first step is simply to check with your HR or payroll team. Most companies do offer VPF, although they can differ a little in how they manage it.

- If your company supports it, you’ll usually just need to submit a request, sometimes it’s a form, sometimes just an email, mentioning how much you want to contribute.

- Once your request is processed, the amount you’ve chosen will start getting deducted from your salary every month, along with your regular EPF contribution.

How Employees Opt In Via Employer ?

While all these three help you build savings for the future, they’re quite different in how they work.

Parameter | VPF | PPF | NPS |

Eligibility | EPF members | Any Indian resident | Indian citizens aged 18-70 |

Contribution | Voluntary | Voluntary | Voluntary |

Employer Contribution | No | No | Optional (Corporate NPS) |

Returns | EPF interest rate | Government-notified interest | Market-linked |

Risk | Low | Low | Moderate |

Lock-in | Until retirement (subject to withdrawal rules). | 15 years | Until retirement (with partial withdrawal provisions). |

Tax Benefits | Eligible under Section 80C deduction (old regime). | Eligible under Section 80C. | Tax Benefits under Sec 80CCD(1), 80CCD(1B) and 80CCD(2). |

Best For | Employees wanting extra retirement savings. | Long-term savings | Higher retirement wealth with market exposure. |

Common Mistakes to Avoid While Making a VPF Contribution

- Assuming your employer will match your extra VPF contribution. Employers only put money into the standard EPF part; they don’t put money into the voluntary portions.

- It is not a good idea to contribute more than you can afford. A greater VPF contribution saves more for your retirement, but you will have less money to keep.

- Not taking into account the necessity for funds. The VPF is not for short term usage and money cannot be withdrawn as easily as one withdraws money from a savings account. Always have an emergency fund on hand at all times.

- Not thinking about the tax effects. If you contribute more than a certain amount, the interest on the extra money may be taxed.

- You can set your payment once and forget about it. Because your finances change over time, you should check your VPF contribution and make changes as needed.

VPF Contribution: A Simple Way to Build Retirement Savings With Prashasthi Corporate

A VPF contribution is one of those simple decisions that can quietly make a big difference over time. If you’re already earning and want to save a bit more without getting into complicated investments, this fits well. It gives you steady growth, tax benefits, and keeps things low-risk. The only thing to watch is how much you’re putting in, don’t stretch your monthly budget too much. Not every plan needs to be aggressive to work. Sometimes consistency does the job better. If you’re unsure how it fits into your overall finances, Prashasthi Corporate can help you figure it out in a practical way.

Disclaimer: This article is for general informational purposes only and does not constitute financial, tax, or legal advice. EPF/VPF rules, interest rates, and tax provisions are subject to change by EPFO and the Government of India. Please verify current rules on epfindia.gov.in or consult a qualified advisor, such as Prashasthi Corporate Advisors, before making financial decisions.