You can invest much more money into your business if you pay less tax. A lot of private limited companies in India pay more than they should, but not because the law makes them to. But because they didn’t prepare ahead of time.

Tax planning management is not just for big companies with lots of cash in bank accounts. It is also possible for small businesses and growing companies to lower their tax bills, too. This can help their cash flow and keep them from rushing to the files at the last minute.

When it comes to taxes, smart planning can make or break a business. This blog post will explain the difference between tax planning and tax management and will also give you some useful examples to apply in real-life scenarios.

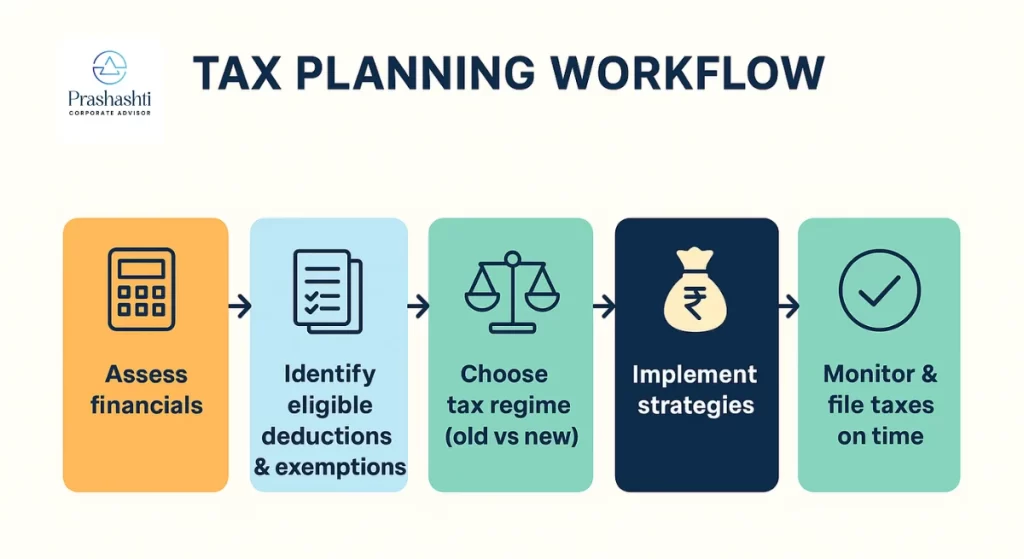

What Is Tax Planning Management?

Tax planning management means arranging your company’s financial movements in a way that reduces the tax liability while also following the law. It is not about evading tax. Instead, it is about using government-approved methods like deductions, exemptions, as well as rebates.

For example, if a company invests in R&D, there are certain expenses that can be claimed as deductions. Similarly, spending on employee benefits or contributing to retirement funds can also reduce taxable income.

Why Private Limited Companies Need It?

A private limited company in India is taxed at 22% (plus surcharge and cess) under the new corporate tax regime if it does not take any exemptions. That’s a really big profit. And without a strategy, the taxes can eat up your capital growth. See corporate tax breakup for different company types for a detailed breakdown.

Here are some reasons why tax planning is important:

- Stable cash flow: Companies can plan ahead and estimate how much they will pay in taxes. You can have no last-minute surprises.

- Business growth: You can use the money you saved on taxes to hire more people to run your business or start new projects.

- Compliance: You can file your taxes correctly and on time to avoid fines, interest, as well as legal problems.

- Investor trust: The companies that follow the rules are more likely to get investors because they show that they are honest.

Corporate Tax Planning and Management

In business tax planning and management, we’re not just talking about lowering taxes. This also includes keeping track of when and how the taxes are paid, by using all the available options, as well as making sure that the tax plan fits with the goals of the business.

For example, a company may choose between the old tax regime (with exemptions) and the new simplified regime. Each option has its pros and cons, and good planning helps in picking the right one.

Corporate tax planning also involves:

- The transfer of pricing rules (important for companies with international operations).

- Minimum Alternate Tax (MAT) calculations.

- Dividend Distribution Tax changes (DDT removed in 2020, now taxed in shareholders’ hands).

- The GST input tax credit management.

A company that ignores these points may pay extra tax or lose credits they are legally allowed to claim.

| Criteria | Old Tax Regime | New Tax Regime |

|---|---|---|

| Base Rate | 25% (domestic companies with turnover < ₹400 cr) | 22% (all domestic companies) |

| Exemptions | Available (e.g., R&D, Section 80 deductions) | Not allowed |

| Effective Rate with surcharge & cess | ~26–29% | ~25.17% |

| Flexibility | More deductions, suited for companies with high eligible expenses | Simplified, suited for companies with fewer deductions |

| Best For | Established businesses leveraging exemptions | Startups and firms seeking lower compliance burden |

Tax Planning and Tax Management Difference

Many people confuse these two terms.

- Tax planning: It’s about strategy. It’s proactive. Used to decide in advance how to reduce tax legally. For example: Choosing depreciation methods or claiming R&D deductions.

- Tax management: It’s about execution. It’s reactive. Used to file returns, pay advance tax, keep records, and respond to notices.

In short, planning is about “what to do,” while management is about “how to do it.” Both are equally important and companies cannot rely on one and ignore the other.

Tax Planning Examples for Private Limited Companies

Let’s look at some practical tax planning examples:

- Depreciation advantages: Are you getting new equipment? Section 32 says you can claim a loss.

- Benefits for startups: For three years in a row, the eligible startups can earn a tax discount under Section 80-IAC.

- Concern for workers: You can deduct contributions to the EPF, gratuity funds, or medical insurance fees for employees.

- Business expenses: Travel, rent, salaries, and professional fees can all be claimed if its directly linked to the business.

- R&D expenditure: Companies which are engaged in research can also claim deductions.

These are all legal methods. They encourage businesses to grow while still fulfilling the tax responsibilities. These are all legal methods. To understand how these deductions affect your tax bill, see our guide on how to calculate income tax for businesses in India.

Recent Updates in Corporate Taxation (2025)

- As per the Union Budget of 2024-25, the government is focusing on simplifying compliance for all the startups and MSMEs. This faceless assessment system continues to reduce red tape.

- GST changes can now allow businesses to claim ITC faster and also improving the working capital.

- Companies can now file updated returns within two years from the end of the assessment year.

- The corporate tax rate for new manufacturing companies remains at 15% (if incorporated before March 31, 2024, and starting production before March 31, 2025).

These updates show why businesses should stay alert. One missed change can mean higher tax outflow or even penalties.

Long-Term Benefits of Tax Planning

The main goals of private limited businesses are tax planning and management because these have long-term benefits such as:

- Every year, you pay less in taxes.

- Checks are easy because the records are in order.

- The ability to use government grants and loans.

- Better name in the business world.

Credibility Check: What Experts Say

“Tax planning is not about avoiding taxes. It’s about being smart enough to use the opportunities the law already gives you,” says a recent report from the Institute of Chartered Accountants of India (ICAI).

The Ministry of Finance has also said that India’s tax system is set up to reward the companies that follow the rules and punish those that don’t. A well-planned business not only saves money but also stays out of needless lawsuits.

Future-Proofing Your Business with Smart Tax Planning Management

India’s tax rules are very complicated and they change all the time. A business that takes tax preparation seriously not only saves money, but it also earns a reputation for being honest and following the rules. Every choice you make, including claiming deductions, picking the correct tax system, or keeping track of GST credits. It all adds up.

CFO’s Tax Planning Checklist for 2025

Before filing, compare the old and new tax regimes.

Make the most of your deductions for R&D, employee benefits, EPF, insurance, and depreciation.

To prevent losing claims, keep track of GST input credits on a monthly basis.

Reduce interest penalties by filing your advance tax on time.

Keep accurate records for evaluations and audits.

Keep an eye on updates from CBDT circulars and the Union Budget.

To maximize strategy, consult a corporate tax consultant.

Therefore, companies like Prashasthi Corporate work with businesses all over India to make compliance easier and also help with financial planning. When you work with the proper consultants, you not only fulfil deadlines, but you also make better decisions that will help your business grow in the coming future.

FAQs

Planning your taxes means finding a way to give you a lower tax bill. Managing taxes means getting things done, like sending in and paying taxes on time.

Yes. Even small companies can reduce liability through deductions on rent, salaries, depreciation, as well as get startup benefits.

Yes. It is legal as long as you follow government-approved rules. However, tax evasion is illegal.

They may pay higher taxes, face penalties for late filing, or miss out on available deductions and exemptions.

Related

Discover more from Prashasthi Corporate Advisors

Subscribe to get the latest posts sent to your email.

Pingback: Difference Between Bookkeeping and Accounting: A Complete Guide | Prashasthi Corporate Advisors

Pingback: How to Calculate Income Tax for Businesses in India (2025)

Pingback: Tax Audit vs Statutory Audit: Key Differences Explained

Pingback: Why Businesses in India Need Virtual CFO Services?

Pingback: Tax Audit Requirements in India: Limits, 5% Rule & Key Mistakes

Pingback: OPC Registration in Bangalore (2025) | Complete Cost Breakdown

Pingback: Corporate Tax in India: Rates & Breakup by Company Type

Pingback: How to Calculate Income Tax for Businesses in India (2026)

Pingback: Legal Compliance Checklist for Private Limited Company in Bengaluru (2026)