Once a finance manager of a group firm accepted a loan assuming it was only an internal adjustment. No big deal, right? Then weeks later, during an audit, questions started coming in. Was the board approval taken? Were the limits checked? Was it even allowed? Something that was just a small decision suddenly turned into a compliance headache.

This is where section 186 of the Companies Act, 2013 comes into play. It lays forth explicit regulations for loans, guarantees, securities and investments so corporations do not move funds casually without sufficient checks. It’s not about limiting a business but it’s about ensuring that decisions are handled carefully and documented properly.

In this blog, we’ll walk through what Section 186 actually means, when it applies, what approvals are needed, and how companies can avoid getting into trouble in the first place.

What Is Section 186 of the Companies Act, 2013?

In simple terms, Section 186 of the Companies Act, 2013, lays down the boundaries within which a company can lend, invest in another company, or support the borrowing of third parties by way of guarantee or security.

It just simply makes sure that they go through a correct process, including acquiring approvals, being under certain restrictions and keeping records. The concept is really simple: corporate money should be spent correctly and big financial decisions shouldn’t be taken randomly.

You can read the exact statutory text of Section 186 on the Ministry of Corporate Affairs’ official portal (mca.gov.in) or on the government’s official legislative repository, India Code (indiacode.nic.in)

Key Takeaways

- Section 186 deals with loans, guarantees, securities, and investments between companies.

- There are limits on how much a company can lend or invest.

- Most deals require Board approval.

- Good records and disclosures are not optional. They are required.

- An illegal loan granted under Section 186 can be rendered null and void by NCLT, and this has been settled through various decisions of tribunals during the period of 2024-2025.

- The amendment of the exemptions framework for Section 186(11), which occurred in November 2025, was carried out by MCA.

Purpose of Section 186

This means that firms can’t just move money from one place to another without thinking about the consequences. Directors can’t just sign off on inter-corporate loans or investments without thinking about whether they are good for the company.

It also brings transparency. Every big transaction leaves a record, so if someone wants to look at it later (auditors, shareholders, regulators), they can plainly see what was done and why.

Who Should Understand Section 186?

This isn’t just for lawyers or compliance teams.

- Directors need to understand it before approving anything.

- Finance teams need it to calculate limits and check approvals.

- Company secretaries handle the paperwork and compliance side.

- Business owners should know the basics, so they’re not blindly relying on others. Understanding these compliance requirements from the beginning is especially important for entrepreneurs planning a company registration in Bangalore, as statutory obligations under the Companies Act apply from the early stages of a company’s operations.

Compliance isn't just about approvals, it's about making informed decisions.

What Transactions Are Covered Under Section 186 of Companies Act 2013?

Section 186 mainly covers four types of transactions. They sound similar, but they’re actually quite different.

Transaction | Meaning | Example |

Loan | Money given that must be repaid. | Company A lends ₹50 lakh to Company B. |

Guarantee | Promise to repay if someone else defaults. | Company A guarantees Company B’s bank loan. |

Security | Assets given as backing for someone else’s loan. | Company A mortgages property for Company B. |

Investment | Buying shares or securities. | Company A buys shares in Company B. |

Loans

This is the most straightforward one. A company gives money to another company with the expectation that it will be repaid.

Guarantees

Here, the company isn’t giving money directly. Instead, it’s saying: “If this company doesn’t repay its loan, we will.” That’s still a financial risk, which is why Section 186 covers it.

Securities

This is similar to a guarantee, but instead of a commitment, the corporation provides assets, such as property, as collateral.

Investments by Subscription or Purchase

This includes the purchase of shares, debentures or other securities of another company.

Applicability of Section 186 of Companies Act 2013

Section 186 applies to most companies, but there are some exceptions.

Which Companies Does Section 186 Apply To?

Generally, it is used for:

- Public Companies.

- Private companies.

- Holding company.

- Subsidiaries.

- Government companies (unless specifically exempted).

However, some companies, like banks, insurance companies, housing finance companies, and certain NBFCs, get exemptions when they’re doing these activities as part of their normal business.

Expert Insight: Today, a financial team will accurately compute the limit, but neglect to include a loan issued eighteen months ago that is still due. Or a board resolution is passed but no one checks if an existing loan agreement with a bank required prior authorization before a new inter-corporate loan is disbursed. Our advice to clients is simple: don’t look at a new loan, guarantee or investment in isolation, but look at it cumulatively. Don’t look at the new transaction in isolation, look at it against the running total and your limits. That one habit stops most of the compliance failures you notice in audits.

Section 186 Limits and Approval Requirements

Maximum Loan and Investment Limits

A firm may make loans, guarantees, security or investments up to the maximum of:

- 60% of its paid-up share capital + free reserves + securities premium or 100% of its free reserves + securities premium.

If it wants to go beyond this, it needs shareholder approval. Let’s make that easier with an example:

- Paid-up share capital: ₹10 crore.

- Free reserves: ₹4 crore.

- Securities premium: ₹2 crore.

Now calculate:

- 60% of ₹16 crore = ₹9.6 crore.

- 100% of ₹6 crore = ₹6 crore.

Since ₹9.6 crore is higher, that becomes the limit. Anything beyond that? You’ll need shareholders to approve it.

When Is Board Approval Required?

Almost every transaction under Section 186 needs Board approval. And not just a casual approval, it has to be discussed and passed in a proper Board meeting.

When Is Shareholder Approval Required?

If the firm exceeds the prescribed limit, it has to gain approval of the shareholders via a Special Resolution.

Prior Approval from Financial Institutions

If the company has borrowed money from banks or financial institutions, those agreements may demand permission before certain transactions are made. So it’s always a good idea to check existing loan agreements first.

Interest Rate Requirements Under Section 186

If a company gives a loan, the interest rate should not be lower than the yield of a Government Security with a similar tenure. Giving loans at very low rates could harm the company’s financial interests.

The MCA has also clarified (General Circular 06/2015, dated 9 April 2015) that where the effective yield on tax-free bonds is greater than the prevailing yield of the closest-tenor Government Security, this does not violate Section 186(7). Similarly, MCA Circular 04/2015 (10 March 2015) clarifies that loans/advances to employees (other than managing/whole-time directors, who fall under Section 185) are not governed by Section 186, provided they follow the company’s employee service conditions and remuneration policy.

Expert Insight: One of the most frequently missed compliance items in our audit engagements is the interest-rate benchmark, corporations have the limitations and permissions right but price an inter-corporate loan below the applicable G-Sec yield without documenting the reason why. Incorporate a basic quarterly check against the RBI’s published G-Sec yield curve into your loan review process, rather than fixing the rate and forgetting about it.

Regulatory Updates: What's Changed (2025-2026)

Here’s what actually changed:

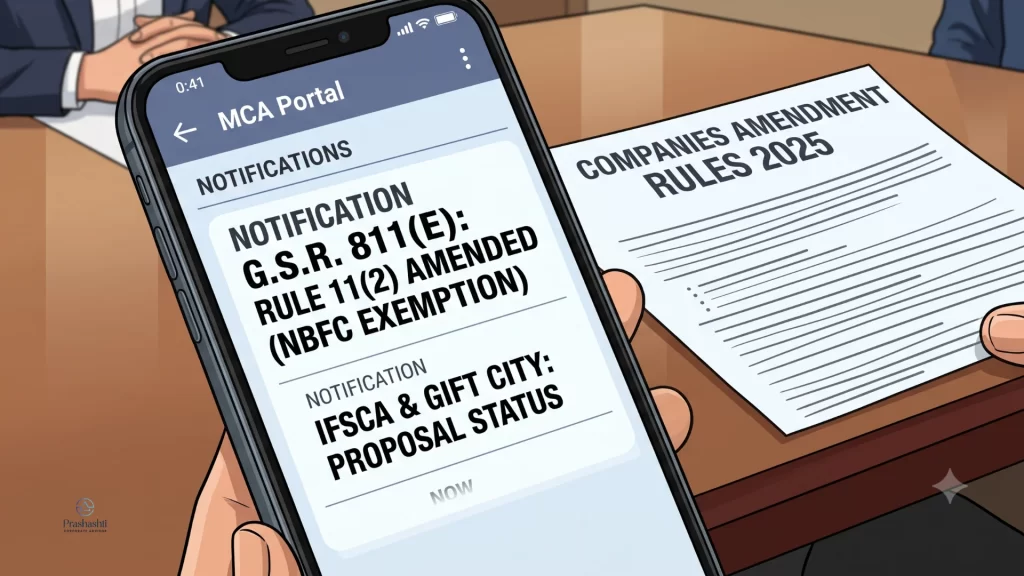

- Under Notification No. G.S.R. 811(E), dated 3rd November, 2025, the MCA has notified the Companies (Meetings of Board and its Powers) Amendment Rules, 2025, in exercise of powers conferred by Sections 173, 177, 178, 186 and 469 of the Act. This is the amendment to 2014 Rule 11(2) regarding the definition of “business of financing industrial enterprises” for exemption under Section 186(11)(a). Banks, insurers, housing finance companies and those companies financing industrial enterprises or providing infrastructural facilities are exempt from Section 186 restrictions and procedures.

Practical effect: if your company (or a group entity) is structured as a financing/NBFC arm, this amendment directly affects whether your inter-group lending needs Section 186 board/shareholder approval at all. Verify current applicability on the MCA Notifications & Circulars page before relying on the exemption.

- A Public Notice floated on 26 June 2025 floated an MCA proposal to extend the Rule 11 exemption available to RBI-registered NBFCs to Finance Companies registered with the International Financial Services Centres Authority (IFSCA), to create equality for entities operating out of India’s IFSCs such as GIFT City. Financial partners in GIFT City should keep a tab on the MCA website and not consider it as finalised.

- The larger trend regarding the MCA reforms up to 2026, which include changes to annual filing deadlines, DIN KYC cycles, and strike-off criteria, shows that there is more ease in procedures for small and dormant companies. However, this does not mean that there is any relaxation on the thresholds of Section 186. It only means that there will be more ease in other filing procedures under the Act.

Disclosure and Record-Keeping Requirements

Getting approvals is just one part of the story under Section 186. What really matters in the long run is how well a company keeps track of what it has done.

Register of Loans, Guarantees, Securities, and Investments

Every company covered under Section 186 is required to maintain a register for these transactions. It’s like a detailed logbook. This register should capture basic but important details like:

- who the money or support was given to,

- how much was involved,

- when it was approved, and

- why the transaction was made.

Financial Statement Disclosures

Besides maintaining internal records, corporations should also make disclosures in their accounting reports where applicable. This would help the stakeholders to know how their resources are being used by the organization. Clear disclosures build trust and reduce unnecessary questions later.

Board’s Report Requirements

In some cases, details of these transactions also need to be mentioned in the Board’s Report. Good reporting reflects good governance, and that matters more than most people realise.

Exemptions Under Section 186 of Companies Act 2013

While Section 186 applies to most companies, the law recognises that for some businesses, lending and investing is part of their everyday operations. So, certain exemptions are provided.

Entity | Exemption |

Banking companies | Loans and investments made in the ordinary course of business. |

Insurance companies | Investments made as part of normal business operations. |

Housing finance companies | Certain transactions carried out in the ordinary course of business. |

NBFCs | Specified loans and investments made as part of their principal business |

Certain Government companies | Exemptions available under notified conditions. |

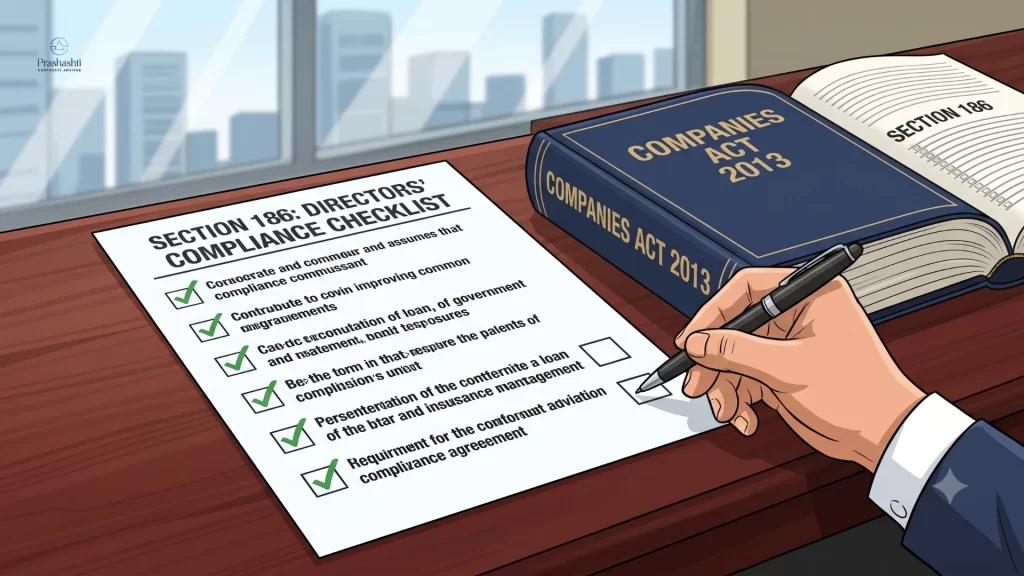

Section 186 Compliance Checklist for Directors

Here’s a basic checklist that will help:

- See if Section 186 is applicable to the transaction.

- Look at the company’s existing loans, guarantees, securities, and investments.

- Confirm whether the new transaction stays within the prescribed limits.

- Obtain proper board approval for loans or investments.

- In case of a limit being exceeded, then the approval of the shareholders is mandatory.

- Is the approval of the bank/financial institution required?

- Make sure the minimum interest rate requirement is satisfied.

- If approved, then modify the statutory record.

- Ensure proper disclosure in the financial statement and Board of Directors’ Report.

Practical Examples of Section 186 Compliance

Sometimes it’s better to learn things by seeing them in real life rather than just learning the rules.

Example 1: Loan to a Subsidiary Company

Let us assume a manufacturing corporation wants to give a loan of ₹3 crore to its subsidiary for expansion.

Before that, the finance team examines if this sum is within the section 186 limits. Once confirmed, the Board authorizes it, the transaction is recorded and disclosures made.

Example 2: Investment Beyond the Limit

A corporation wants to invest in another business. After calculating everything, the company realizes that the investment will violate the authorized limit.

It needs shareholder approval by way of Special Resolution first, rather than push ahead. Only then does it continue.

Section 185 vs Section 186: Key Differences

These two sections often get mixed up, but they deal with different things.

Basis | Section 185 | Section 186 |

Purpose | Deals with loans to directors and connected parties. | Regulates loans, guarantees, securities and investments of enterprises. |

Applicability | Directors and specified related entities. | Companies making loans, guarantees, securities, or investments. |

Transactions Covered | Loans, guarantees, and securities involving directors. | Loans, guarantees and securities and investments in other companies. |

Approval Requirements | Depends on the nature of the transaction. | It requires board approval and in some situations shareholder approval. |

Limits | Restrictions under Section 185. | Prescribed financial limits under Section 186. |

Exemptions | Limited exemptions. | Exemptions available for specified companies and transactions. |

Common Compliance Mistakes Under Section 186

- One common mistake is crossing the Section 186 limits without realising it. Companies sometimes look only at the new transaction and forget to include earlier ones.

- Another issue is charging interest below the required rate. Even if both parties agree, the law still expects a minimum benchmark.

- Then there’s documentation. Missing entries in registers, partial disclosures or poorly managed data might generate complications in audits.

- And finally, approvals. Sometimes decisions are taken informally without proper Board resolutions. That can become a serious issue later.

Penalties for Non-Compliance with Section 186

Penalties for the Company

If a company doesn’t follow the provisions, it can face penalties under the Companies Act. Apart from fines, repeated issues can attract closer scrutiny from regulators.

Penalties for Officers in Default

Directors and officers involved in the decision can also be held responsible. That’s why approvals shouldn’t be taken lightly.

Practical Consequences Beyond Monetary Penalties

Beyond penalties, non-compliance can create practical problems:

- delays in funding,

- issues during due diligence,

- audit remarks, and

- loss of credibility with lenders and investors.

Section 186 of Companies Act 2013: Keeping It Simple with Prashasthi Corporate

Most companies don’t get into difficulty because they wish to disobey the laws when it comes to section 186 of the Companies Act 2013. Usually it is something really small that gets ignored. A limit isn’t checked, an approval is delayed, or records aren’t updated on time. These things add up.

The good part is, once you understand how the section works, it’s not that complicated to follow. A little attention at the right stage can save a lot of stress later. And if you ever get stuck or need guidance with approvals, documentation, or ongoing compliance under Section 186, seeking professional corporate advisory services can help ensure your transactions remain compliant with the Companies Act while reducing regulatory risks.

Disclaimer: This article is for general informational purposes and does not constitute legal advice. Section 186 case law is evolving, and specific facts materially affect outcomes. Consult a qualified company secretary or corporate lawyer before relying on any interpretation above for a live transaction.