Most people notice PF only when salary slips arrive or when they switch jobs. But very few actually understand how it works behind the scenes, especially the PF contribution of the employer. That’s where confusion starts.

Is your employer paying the right amount every month? Why is part of your PF going into a pension fund you can’t touch easily? And what happens if your salary is more than ₹15,000? Does PF stop increasing?

These are not small questions. Your PF is long-term money. Tiny misunderstandings today can turn into big gaps at retirement.

This blog breaks down the employer PF contribution rules in simple words with real examples, and the latest updates, so you actually know where your money is going, and why it matters.

Flash Update: Jan 2026

The Supreme Court has officially ordered the government to decide on increasing the wage ceiling (from ₹15,000 to ₹21,000/₹25,000) within the next four months. This will drastically change the Employer Contribution split for millions of employees by mid-2026.

What Is Provident Fund (PF) and Why the Employer’s Contribution Matters?

In India, the Employees’ Provident Fund Organisation (EPFO) manages a way for workers with a salary to save for retirement. In this plan, the employee and company both pay the same percentage of the employee’s basic salary and dearness allowance (DA) every month.

These monthly payments will add up over time to form a retirement fund that can be used after leaving a job, when someone retires, or in some situations.

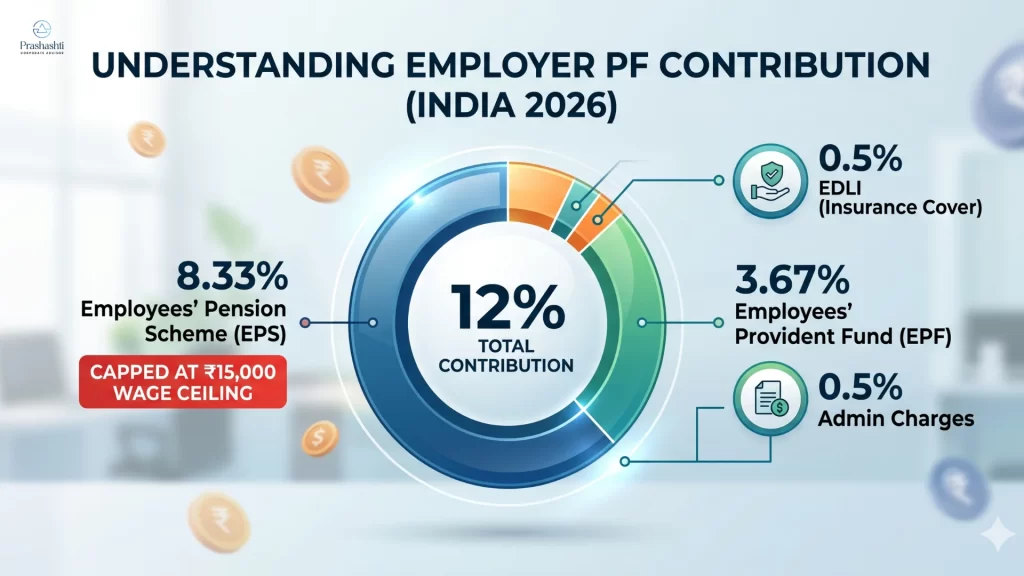

The employer’s mandatory share is what we mean when we discuss the PF contribution of the employer. This contribution is not just extra savings for you. It is split across three components:

- EPF (your retirement savings)

- EPS (pension)

- EDLI (insurance coverage)

Understanding this split is important because not all of the employer’s contribution is available for direct withdrawal.

| Component | Rate | Based On | Paid By |

|---|---|---|---|

| Employer EPF | 3.67% | Basic + DA | Employer |

| EPS | 8.33% | Basic + DA (capped at ₹15,000) | Employer |

| EDLI | 0.5% | Basic + DA (capped at ₹15,000) | Employer |

| EPF Admin Charges | 0.5% | PF wage | Employer |

| EDLI Admin Charges | NIL (removed) | – | Employer |

| Total Employer Outflow | 13% – 14% approx. | Depends on wage | Employer |

When PF Contribution Becomes Mandatory for Employers (Eligibility Rules)?

Under EPFO rules, organisations with 20 or more employees are required to register and contribute to PF for eligible employees. If your business is still not PF registered, contact our PF consultants in Bangalore.

Smaller establishments (with fewer than 20 employees) may get certain relaxations. In some cases, they may contribute at a reduced rate of 10% instead of 12%, depending on the industry and financial condition.

If your employer has 20 or more employees, PF contribution is compulsory. If not, it depends on whether the employer has voluntarily opted into the scheme. Want to know whether your business must register under EPFO? Check our detailed guide on PF Registration Eligibility Criteria in India

What Is the Current Mandatory PF Contribution of Employer Rate in India?

This is how the PF contribution of the employer works under the current EPFO rules:

- Contribution rate: The employer must contribute 12% of the employee’s basic salary plus dearness allowance (DA) every month.

- How the employer contribution is split: The employer’s 12% is divided as follows:

- 3.67% goes into the employee’s EPF (Provident Fund savings)

- 8.33% goes into the Employees’ Pension Scheme (EPS)

-

0.5% : EDLI

-

0.5% : Administrative Charges

Wage ceiling for pension: The EPS portion is calculated on a maximum wage of ₹15,000 per month. Even if basic + DA is higher, pension contribution remains capped unless the employer opts for a higher voluntary contribution.

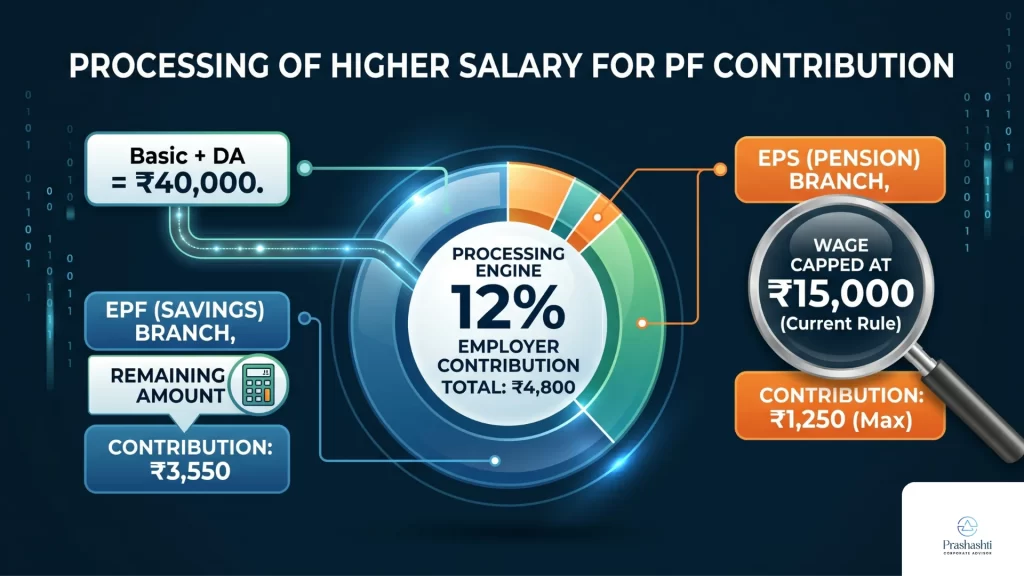

PF Contribution Example (Salary ₹40,000)

Basic + DA = ₹20,000

Employer 12% = ₹2,400

EPS = ₹1,250 (8.33% of ₹15,000 capped)

EPF = ₹1,150

- Additional employer costs: Apart from the 12%, the employer also pays:

- EDLI (insurance) contribution.

- EPF and EDLI administrative charges.

These are paid by the employer and are not deducted from the employee’s salary.

- A timely monthly deposit is mandatory: Employers must deposit both employee and employer PF contributions within the prescribed timelines, and delays can attract interest and penalties.

Moreover, these rules decide how much can go into your savings, pension, as well as insurance every month. For organisations managing both PF and ESI compliance, here is a full breakdown of ESI registration online.

How to Calculate PF Contribution of Employer for a New Employee?

Step 1: Identify Basic + DA

Step 2: Apply 12% on Basic + DA

Step 3: Split 12% into:

-

8.33%: EPS (capped at ₹15,000)

-

Remaining: EPF

Example (New Joiner):

Basic + DA = ₹18,000

Employer 12% = ₹2,160

EPS = 8.33% of ₹15,000 = ₹1,250

EPF = ₹910

Employer PF Contribution Breakdown on a ₹15,000 Salary

| Contribution Type | Percentage | Amount (on ₹15,000 salary) |

|---|---|---|

| EPF Contribution | 3.67% | ₹550.50 |

| EPS (Pension) Contribution | 8.33% | ₹1,249.50 |

| EDLI Contribution | 0.50% | ₹75.00 |

| Total Employer Outflow | 12.50% | ₹1,875.00 |

PF Contribution of Employer vs Employee: Key Differences

This table helps clearly show the difference between the PF contribution of the employee and the employer.

Component | Employee Contribution | Employer Contribution |

Rate | 12% of basic + DA | 12% of basic + DA |

Goes to EPF | 100% | 3.67% |

Goes to EPS | No | 8.33% (capped) |

Insurance & admin | No | Paid by employer |

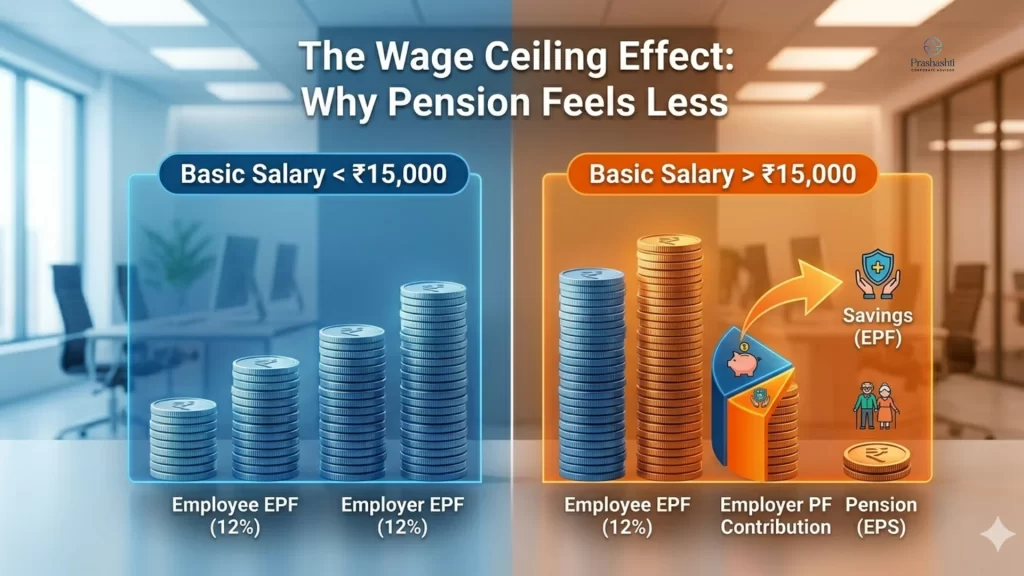

What Wage Ceiling Means And Why Pension Looks Limited?

Even though the employer contributes 12%, the pension part is calculated on wages capped at ₹15,000 per month.

So if your basic + DA is ₹30,000:

- Pension (EPS) is still calculated on ₹15,000.

- The remaining employer contribution flows into EPF savings.

This is why high-salary employees often notice larger EPF balances but relatively modest pension benefits.

There have been discussions about increasing the wage ceiling (to ₹21,000 or more), but as of mid-2025, ₹15,000 remains the official limit.

Interest, Pension, Withdrawal & Insurance Explained Simply

- EPF savings earn interest: For FY 2024-25, EPFO declared an interest rate of 8.25% per annum.

- Interest is added yearly, and your balance grows with contributions + interest combined.

- EPS provides pension benefits after retirement, based on years of service and eligible wages.

- EDLI insurance offers life cover linked to PF membership. If an employee passes away while in service, the nominee may receive insurance benefits.

So, PF is not just savings. It is a combination of savings, pension, and insurance backed by both employer and employee contributions.

EPFO 3.0 & Auto-Mode Settlements: Get Your Money in Hours

- In 2026, 95% of advance claims are now settled via Auto-Mode. Unlike previously it used to take 7–20 days. The auto-settlement limit for advances has been increased to ₹5 Lakhs. The interesting thing is if your data matches, the system approves the payment automatically without manual review

- As part of the 3.0 rollout, plans to allow members to withdraw up to 50% of their balance directly via integrated apps or specific cards for emergencies. Further, for small corrections like name, date of birth errors, you don’t need to follow up repeatedly with your employer, these are done via OTP-based self-attestation on the portal.

- However, with AI sometimes you might get rejected by the systems for small errors. Example : Your name on your Bank Account must match your UAN exactly. (e.g., “Arun K” vs. “Arun Kumar” will trigger a rejection).

- Under new 2026 guidelines, members are encouraged to maintain a 25% minimum balance to preserve their retirement corpus, even when taking multiple advances.

How To Calculate a Pension? EPS Pension Calculation Formula

To understand what your pension may look like, here is the actual EPFO formula:

Pension = (Pensionable Salary × Pensionable Service) / 70

Where:

Pensionable Salary = average of last 60 months (capped at ₹15,000)

Maximum pensionable service = 35 years

Example:

If pensionable salary = ₹15,000

Service = 30 years

Pension = (15,000 × 30) / 70

= ₹6,428 per month approx.

This helps employees understand why EPS pension is usually modest.

| Scenario | Pensionable Salary | Service (Years) | Monthly Pension |

|---|---|---|---|

| Case 1 | ₹15,000 | 10 | ₹2,142 |

| Case 2 | ₹15,000 | 20 | ₹4,285 |

| Case 3 | ₹15,000 | 30 | ₹6,428 |

| Case 4 | ₹12,000 | 25 | ₹4,285 |

To understand whether your company qualifies for PF and how eligibility rules apply, refer to our complete guide on PF registration eligibility

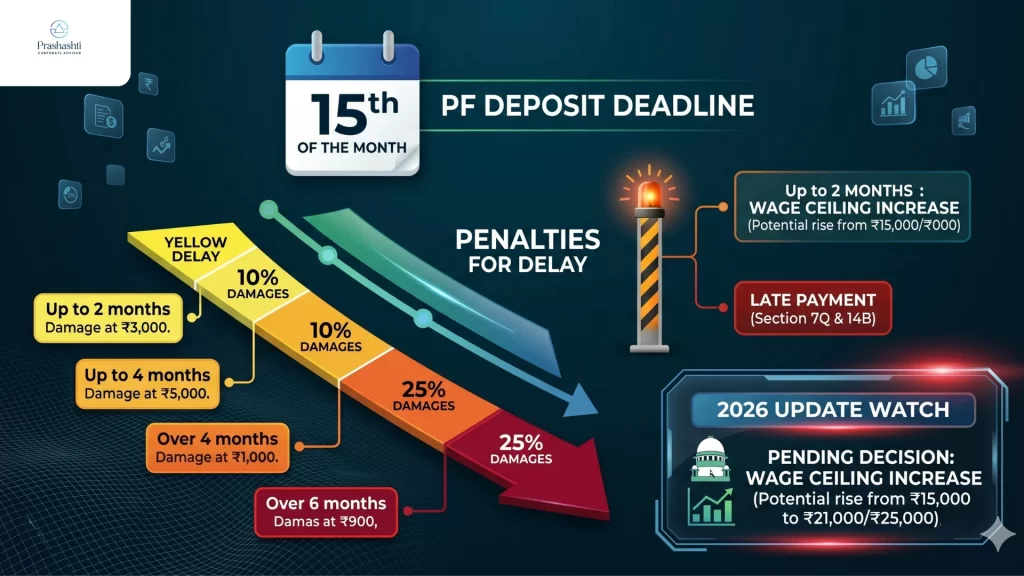

Penalties for Late Deposit of Employer PF Contributions

Contributions to the PF must be deposited by the 15th of the subsequent month at the latest.

Under Section 7Q, late payments are subject to interest at a rate of 12% annually, computed from the due date until the actual payment date.

Section 14B allows for the imposition of damages based on the delay period in addition to interest.

Delay of two to four months : 10% damages

Delays of four to six months: 15% damages

Over six months of delay = 25% damages

Interest is not included in damages, which are assessed separately.

Delays of up to two months result in 5% damages.

How Do Employers Report Their PF Contributions To The Government Portal?

Register on the EPFO Unified Portal.

Generate monthly ECR (Electronic Challan cum Return).

Upload employee wage details.

Verify UAN mapping.

Make payment before 15th of following month.

What’s New in 2026 : What You Should Watch?

- Proposals to increase the wage ceiling, as of January 9, 2026, the Supreme Court has directed the Central Government and EPFO to take a final decision on increasing the wage ceiling (likely to ₹21,000 or ₹25,000) within four months.

- Any increase would raise both employer and employee contribution amounts.

- Until an official notification is issued, existing rules continue to apply.

Employees and employers should track EPFO announcements to stay compliant and avoid surprises. Modern compliance management is evolving rapidly learn how RegTech in India is reshaping PF, ESI, and statutory processes.

Why Some Employees Feel Employer PF Is “Less” Despite Good Salary?

Many employees assume employers always contribute the same amount they do. That’s not fully true.

Because pension contributions are capped, the PF contribution of the employer feels smaller in pension terms, even if EPF savings grow well.

This matters if you are relying on pension income after retirement. Many employees, therefore, supplement PF with voluntary contributions or other retirement investments.

Make Timely PF Payments & Stay Compliant

It takes more than the numbers to understand the PF contribution of an employer. Knowing what your employer adds each month can help you avoid surprises later, especially when it comes to pension as well as the withdrawal benefits.

If you need help understanding PF rules, compliance, and the latest updates, trusted tools like Prashasthi Corporate can help. They explain things in a way that is easy to understand, without using a lot of technical language. Knowing how these payments work today helps you make better plans for tomorrow, which makes your financial future more certain and safe.

Pingback: What is the Minimum Capital Required for Company Registration?

Pingback: Labour Law Compliance in India 2026: New Labour Codes Guide

Pingback: PF Registration Eligibility: Rules, Criteria & Guidelines

Pingback: How to Make Payment of ESIC Online in 2026 (Easy Guide)