When starting a business in India, one of the first questions you’ll get is, “Should I register as a Pvt Ltd, OPC, or LLP?”

That decision is not merely a legal formality. It determines how much tax you’ll pay, how frequently you’ll file returns, how easily you may take revenues, and how funders see your company.

In this blog, we’ll go over the tax treatment of Pvt Ltd vs OPC, vs LLP in layman’s words so you can decide which is best for your business.

Why Tax-Friendly Structure Matters

Every business wants to make a profit. However, how much of that profit you keep is determined by how much you pay in taxes.

Some structures are subject to corporate tax in India, as well as taxation on profit distribution. Others allow you to avoid the dividend tax. Some offer deductions, while others do not.

Then there is compliance. Audits, filings, and timelines. So, whether you’re a solitary founder or a small team, tax complexity can stymie your growth more than you realise.

That is why understanding the tax system for each structure is essential before registering your business.

Pvt Ltd vs OPC vs LLP: What They Mean

Before we dive into taxes, let’s understand what these three structures are. This forms the base of the Pvt Ltd vs OPC vs LLP comparison.

A Private Limited Company (Pvt Ltd) is a company registered under the Companies Act. It requires a minimum of two directors and offers limited liability. Moreover, it’s ideal for businesses that want to scale or attract investors.

A One Person Company (OPC) is similar to a Private Limited Company but is designed for a single founder. It has limited liability and a corporate structure, but only one member.

A Limited Liability Partnership (LLP) combines the characteristics of a partnership and a firm. It is simpler than a Pvt Ltd and more adaptable, particularly for professional service organisations. LLPs do not have shareholders or directors; instead, they have partners.

Pvt Ltd vs OPC vs LLP: Tax Basics at a Glance

Here’s the main difference:

| Aspect | Private Limited Company (Pvt Ltd) | One Person Company (OPC) | Limited Liability Partnership (LLP) |

|---|---|---|---|

| Taxation Basis | Taxed as a separate legal entity under the Companies Act | Same as Pvt Ltd (corporate tax rules apply) | Taxed as a partnership firm under the LLP Act |

| Corporate Tax Rate | ~22% (domestic companies under Section 115BAA); 25% if not availing special provisions | Same as Pvt Ltd | Flat 30% on taxable income |

| Dividend Taxation | Dividend taxable in hands of shareholders (no DDT) | Same as Pvt Ltd | No dividend distribution tax; partners can withdraw profits tax-free |

| MAT (Minimum Alternate Tax) | Applicable at 15% (plus surcharge & cess) | Applicable (same as Pvt Ltd) | Not applicable to LLPs |

| Surcharge & Cess | 7% / 12% surcharge depending on income + 4% health & education cess | Same as Pvt Ltd | 12% surcharge (if applicable) + 4% cess |

| Tax Audit Requirement | Mandatory if turnover exceeds threshold (as per Companies Act & IT Act) | Same as Pvt Ltd | Mandatory if turnover > ₹40 lakhs or contribution > ₹25 lakhs |

| Compliance Cost | High – annual filings, board meetings, audits | Moderate – fewer compliance requirements than Pvt Ltd but more than LLP | Lower – relatively simple filings compared to companies |

Tax for Private Limited Companies

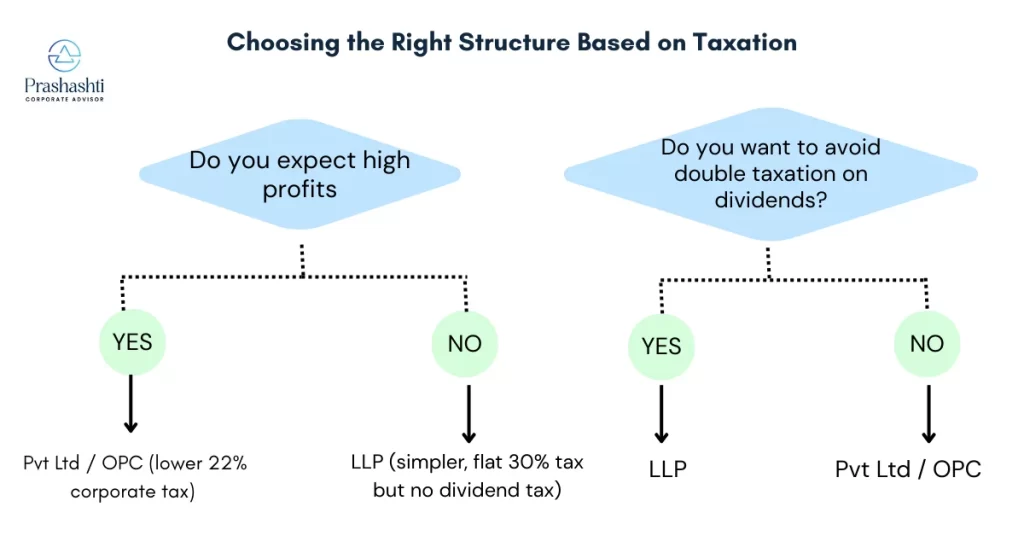

If a Pvt Ltd company chooses the new tax structure under Section 115BAA, it pays 22% (plus cess). This is available to all domestic enterprises with the following conditions: no special deductions, such as Section 10AA exclusions, increased depreciation, or R&D claims.

If the company is freshly incorporated and involved in manufacturing, it may be eligible for the 15% tax rate under Section 115BAB.

However, there is more.

Even after paying corporation taxes, if profits are distributed as dividends, the Dividend Distribution Tax (DDT) has been eliminated since 2020. Dividends are now taxed at the shareholder’s income level.

Another point to consider is MAT (Minimum Alternate Tax). If you do not select for the new tax regime, your book earnings may be subject to MAT at 15% (plus surcharge and cess).

Advantages of Pvt Ltd taxation:

- Optimal for long-term growth and investing.

- Eligible for Startup India advantages and angel tax exemptions.

- Easy to obtain VC or equity capital.

- Losses can be carried forward in certain instances.

Cons:

- Complex compliance requirements, such as audits, director meetings, and MCA filings

- When dividends are withdrawn, there is a dual tax burden.

- In certain cases, MAT is applicable.

In short, if you’re starting a scalable business with future funding plans, the Pvt Ltd route is still tax-effective.

Tax for One Person Company (OPC)

OPC’s tax structure is identical to that of a private limited company. It is likewise taxed at 22% under the new scheme, which follows the same criteria as MAT and dividend taxation.

OPC does not provide any specific tax exemptions or benefits. It is regarded as any other domestic corporation under the Income Tax Act.

So, why should you choose it?

If you are a solitary founder who wants to maintain limited liability and corporate status without adding a second director or shareholder, OPC is the ideal option. Furthermore, it provides a superior structure than a sole proprietorship and can be changed into a Private Limited Company as needed.

Drawbacks of tax for OPC:

- Dividend withdrawal is still taxable

- MAT applies

- It cannot raise venture capital (since only one shareholder is allowed)

In the context of Pvt Ltd vs OPC vs LLP, the tax for OPC gives no major advantage over Pvt Ltd, but it provides structural simplicity for solo founders.

Tax for LLP in India

An LLP pays a flat 30% tax on its total income, plus any relevant surcharges and cess. There is no concept of business tax slabs here, and they are fixed.

So, what distinguishes LLP tax is the handling of profit sharing.

After the LLP pays its 30% tax, partners can take profits without incurring further taxes. No DDT. The partner has no tax liability. That’s a huge advantage for small teams looking to keep their earnings simple.

Even better, MAT does not apply to LLPs.

LLP compliance is also lighter. Audit is only required if:

- Annual turnover exceeds ₹40 lakh, or

- Capital contribution exceeds ₹25 lakh

For many service-based businesses or consultants, that means you can run tax-efficiently without worrying about audits and corporate filings.

Pros of tax for LLP:

- No dividend tax

- No MAT

- Simpler books and returns

- Suitable for smaller or low-cap firms

Cons:

- Cannot raise equity funding

- Tax rate is higher than Pvt Ltd (30% vs 22%)

- Cannot issue ESOPs or bring in shareholders

Pvt Ltd vs OPC vs LLP: Which One Should You Choose?

Choose a Private Limited Company (Pvt Ltd) if:

You intend to recruit outside investors or raise venture capital.

With a well-organized corporate structure, you wish to grow quickly.

Higher compliance costs are acceptable to you in exchange for increased credibility and room for expansion.

Despite the additional taxation layers brought about by dividend distribution, tax planning flexibility is important.

Choose a One Person Company (OPC) if:

As a sole proprietor, you desire the advantages of corporate status.

As your company expands, you anticipate becoming a Pvt Ltd.

You don’t need a co-founder if you want limited liability protection.

You want fewer shareholders but are at ease with taxation similar to that of a PVT LTD.

Choose a Limited Liability Partnership (LLP) if:

You prefer direct profit withdrawal and less complicated taxation (no MAT, no dividend tax).

You concentrate on small businesses, consulting, or professional services.

You would rather have fewer statutory formalities and lower compliance costs.

Funding from external equity is not a top priority.

Still unsure? Talk to experts.

Prashasthi Corporate helps you pick the right structure, register your business, and handle tax compliance, without confusion. Make the right call now to avoid bigger issues later.

Related

Discover more from Prashasthi Corporate Advisors

Subscribe to get the latest posts sent to your email.

Pingback: Annual ROC Filing Checklist for Private Limited Companies